Will Korea’s 2027 Crypto Tax Actually Happen?

Why a “Locked-In” Timeline Is Being Shaken Again

Most crypto investors had been treating January 1, 2027 as the base-case scenario for taxation. Following the December 2024 amendment to the Income Tax Act, crypto taxation was deferred once again, and the National Tax Service (NTS) officially confirmed that taxation would apply to transfers and lending starting from January 1, 2027.

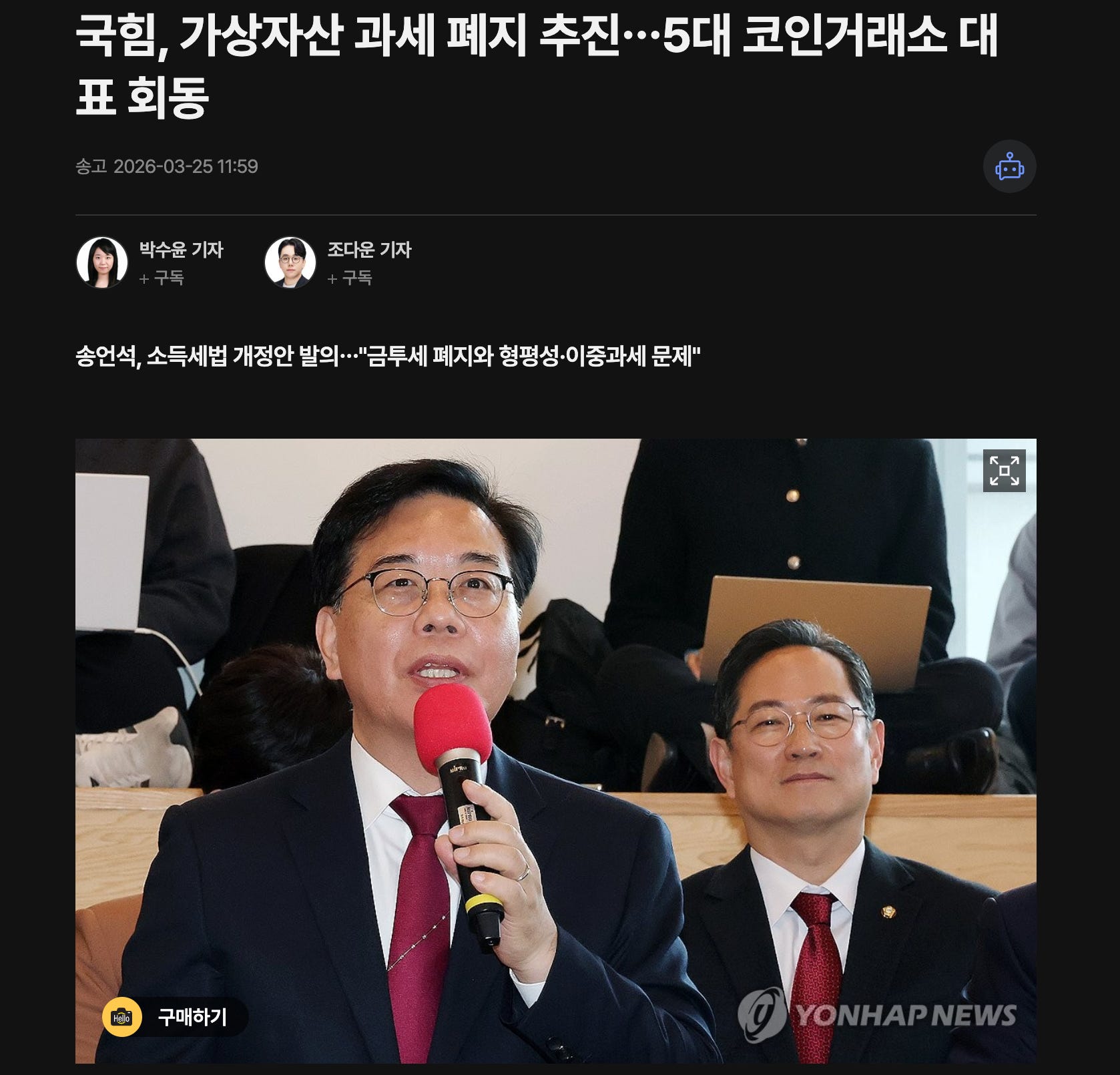

However, sentiment began to shift again from mid-March 2026. The People Power Party proposed a bill to abolish crypto taxation and, on March 25, held a public roundtable with the five major exchanges, bringing the issue back into the political agenda. While the law itself remains in place, the renewed political intervention has led the market to once again question whether another deferral is possible. This is not surprising, as the emergence of political pressure suggests that the system is not progressing in a stable or linear manner.

That said, it is important to clearly frame the current situation. The administrative side continues to operate under the assumption that taxation will proceed, while the political side has begun to apply pressure again. What is needed now is not a simple debate of pros and cons, but an analysis of why political actors are revisiting this issue at this timing, why institutional infrastructure continues to move forward regardless, and what the most realistic outcome is likely to be.

1. Why is the political side revisiting this issue now?

The official justifications presented by policymakers can be summarized as follows:

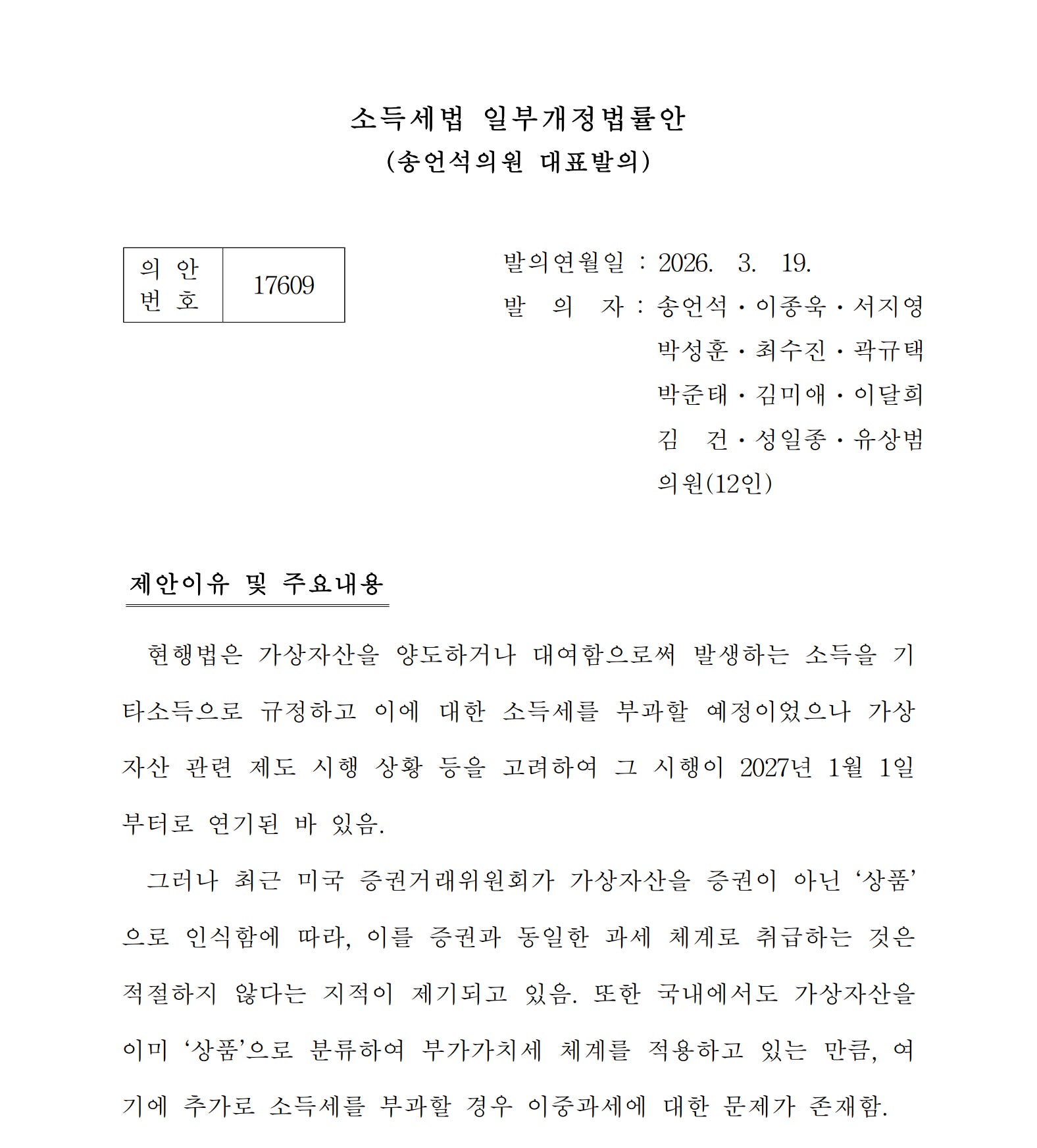

First is fairness. The proposed amendment to the Income Tax Act submitted on March 19 by Rep. Song Eon-seok argues that imposing a separate income tax on crypto assets, while financial investment income tax has been abolished, undermines fairness and consistency in the tax system. The same argument was reiterated during the March 25 roundtable with exchanges. Retail investors, who are not major shareholders, effectively do not pay capital gains tax on domestic equities, yet crypto assets would be subject to a 22% tax. The core framing here is not preferential treatment for crypto, but rather correcting imbalance relative to equities.

Second is feasibility. The same proposal highlights administrative challenges, such as determining acquisition costs for non-resident foreigners. Following the March 25 meeting, policymakers also publicly mentioned concerns raised by the industry, including insufficient preparedness by the National Tax Service and the risk of capital outflows to overseas exchanges. This argument does not rely solely on anti-tax sentiment, but directly challenges the executability of the system. Politically, this framing is effective. Compared to debates around fairness, the question of whether taxation can be properly enforced resonates more broadly, even with non-investors.

Third is political timing and voter considerations. Crypto taxation has already been deferred multiple times, and there is still time before implementation. Challenging it now carries lower political cost than reversing it after enforcement. At the same time, the narrative that “stocks are not taxed, but crypto is” is simple and compelling for retail investors. The fact that the ruling party went beyond proposing legislation and organized a public roundtable with exchange executives suggests an intention to elevate this issue into a broader political agenda. While this is an interpretation rather than a confirmed fact, recent messaging and timing support this view.

However, one important distinction must be made. Political signaling does not necessarily imply a strong conviction to fully abolish taxation. At this stage, while a repeal bill has been proposed and publicly highlighted, the opposition party has stated that internal consensus has not yet been reached. This suggests that the current move is less about final outcomes and more about reopening negotiations. It is therefore premature to interpret current political actions as definitive results.

2. While politics wavers, institutionalization continues

This is the key point. While political actors are revisiting taxation, administrative and institutional preparation is continuing without pause.

The National Tax Service is responsible for implementing and enforcing tax laws passed by the National Assembly. It is not a political decision-maker, but an execution body. Accordingly, the NTS is proceeding under the assumption that taxation will be implemented. It continues to operate a dedicated crypto taxation information page, clearly stating that taxation applies from January 1, 2027, and has already established frameworks for data submission, reporting forms, and reference materials. From an administrative standpoint, this is no longer a “planned system,” but a system actively under preparation.

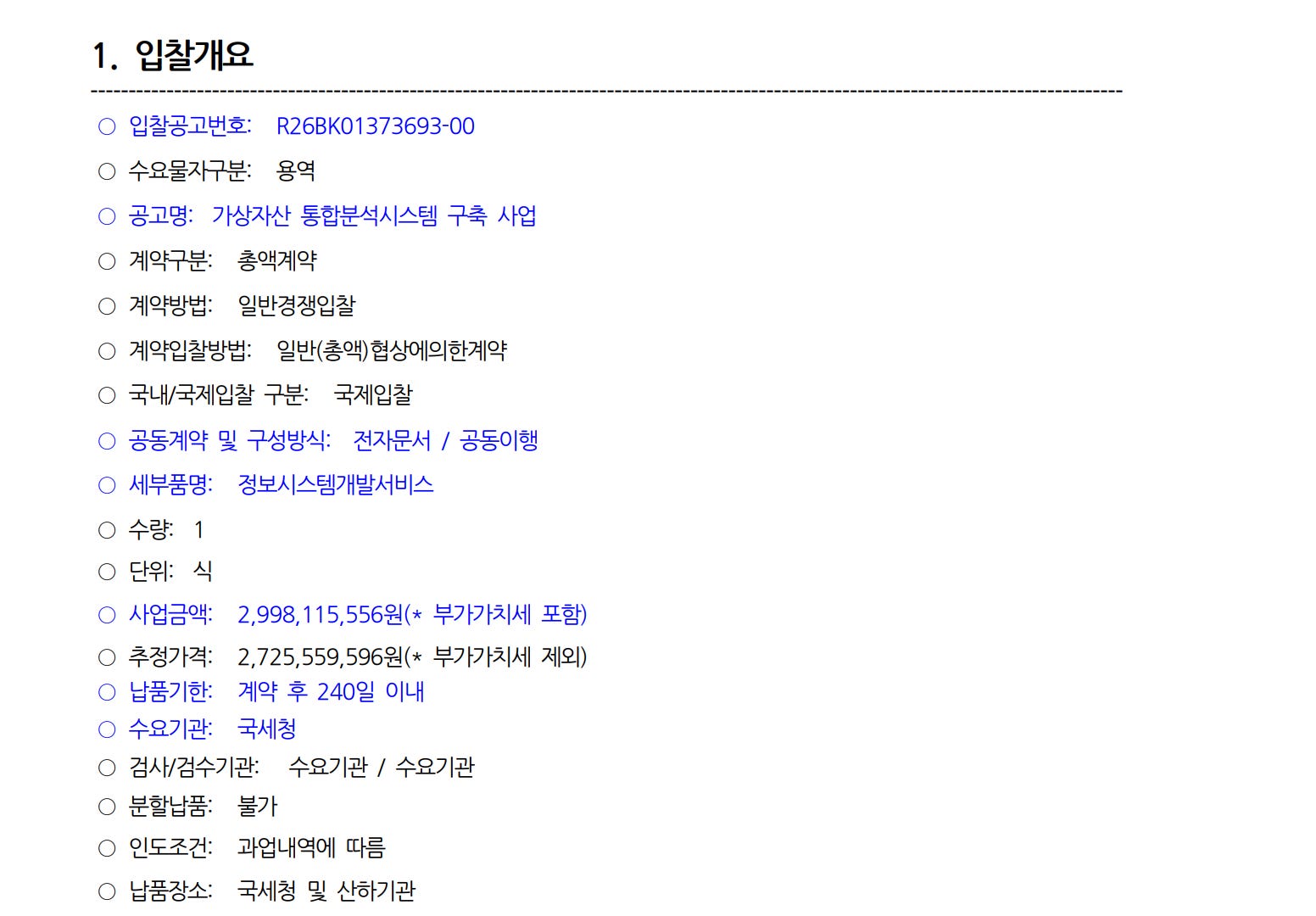

The level of preparation is also concrete. On March 20, 2026, a public procurement notice was posted for the “Integrated Crypto Asset Analysis System” project. The NTS is the contracting authority, with a project budget of approximately KRW 2.998 billion. Proposal submissions are scheduled for April 7 to 9, with delivery required within 240 days of contract signing. This is not exploratory work, but active system development. In other words, while political actors debate whether to proceed, tax authorities are preparing as if implementation will occur.

The broader direction of the NTS aligns with this. In its 2026 operational plan, the NTS emphasized stable tax revenue collection, fair taxation, combating offshore tax evasion, and enhancing data analysis capabilities. While not specific to crypto, this reflects a general approach of strengthening enforcement rather than scaling back planned taxation. Crypto taxation should be viewed within this broader trajectory.

The Financial Services Commission (FSC) also plays a critical role. While it does not directly impose taxes, it determines which entities operate within the regulatory framework and what transaction flows become visible. Under the FSC, the Financial Intelligence Unit (FIU) oversees anti-money laundering (AML), analyzing financial data and supervising compliance. In the crypto market, AML infrastructure effectively makes transactions visible enough for taxation.

According to the FIU’s February 2026 AML plan, strengthening crypto AML systems is a key priority. This includes improving AML frameworks for stablecoin issuers, addressing risks related to overseas operators and self-custodied wallets, and enhancing visibility into transaction flows. While not tax law itself, this infrastructure increases traceability, which is essential for taxation. In other words, while politics questions taxation, financial authorities are simultaneously increasing the system’s ability to support it.

Internationally, the direction is the same. According to OECD documents, Korea is among the countries committed to initiating the Crypto-Asset Reporting Framework (CARF) in 2027. CARF enables automatic exchange of crypto-related tax information between jurisdictions. Once implemented, hiding assets through overseas exchanges will become significantly more difficult. While adoption speeds will vary across countries, the key point is that Korea is already aligned with this global framework. Even if domestic political debate continues, externally, Korea is positioning itself as a taxation-ready jurisdiction.

3. The outcome is likely “modified implementation,” not repeal

The most realistic conclusion at this stage is not full repeal, but modified implementation.

While political momentum for repeal has increased, administrative bodies, financial regulators, and international frameworks are all moving toward 2027 implementation. After establishing data systems, AML infrastructure, and international commitments, abandoning the system entirely would carry significant political and administrative costs.

From a political perspective as well, modification is easier to justify than repeal. Adjustments can be framed as improving fairness or addressing practical concerns. Therefore, the current situation is less about “implementation vs repeal” and more about how the system will be adjusted before implementation.

There are already early signals on what this “modified implementation” could look like.

The most immediate and realistic adjustment being discussed is an increase in the basic exemption threshold. Under the current framework, taxation applies to gains exceeding KRW 2.5 million annually. However, in a March 25 report, Hwang Seok-jin, an advisory member of the Democratic Party’s Digital Asset Task Force, noted that while taxation itself is necessary, the exemption threshold should be raised to at least KRW 20 million.

While this is not an official policy proposal, but rather an expert opinion, it is widely viewed as one of the most practical adjustment levers currently available. In a political environment where fairness relative to equities has become a central issue, maintaining the implementation timeline while raising the threshold offers a way to reduce the burden on retail investors without abandoning the taxation framework altogether.

A second likely adjustment is a more realistic definition of the enforcement scope. The most significant practical challenges today lie in areas that are inherently difficult to track and evaluate, such as overseas exchanges, self-custodied wallets, acquisition cost calculations for non-residents, and complex DeFi transactions. Notably, even the rationale behind the proposed repeal bill points to administrative difficulties, particularly in determining acquisition costs for foreign investors.

Given these constraints, a full rollback of the system appears less likely than a phased approach. A more plausible path would be to first establish clear taxation around transactions conducted through domestically regulated exchanges, while gradually expanding coverage to overseas transfers and self-custodied wallets as data infrastructure and international information-sharing frameworks mature. This is not based on any finalized policy, but rather a reasonable inference based on current institutional limitations and policy debates.

A third area of adjustment is the refinement of rules around acquisition cost and edge-case transactions. The National Tax Service has already acknowledged scenarios where verifying acquisition costs is difficult and has delegated certain criteria to presidential decree. This suggests that the system is not yet fully finalized and still leaves room for further clarification before implementation.

As such, “modified implementation” is unlikely to be limited to raising the exemption threshold alone. It will likely involve more granular rule-setting around acquisition cost calculations, cross-border transfers, and the classification of ambiguous transaction types, ensuring that taxation is not only theoretically defined but also practically enforceable.

4. What will modified implementation likely look like?

Based on recent political signals, administrative preparation, and practical constraints raised by the market, the direction is becoming clearer.

While the ruling party has reopened the debate around fairness, capital outflows, and administrative readiness, the National Tax Service continues to build out its enforcement infrastructure. Politics is wavering, but administration is moving forward. This makes a full repeal unlikely, with the outcome leaning toward modified implementation.

1) Maintain the timeline, but raise the exemption threshold

The most likely adjustment is to keep the 2027 timeline while significantly increasing the exemption threshold. Rather than abandoning taxation, policymakers can address fairness concerns by effectively excluding small and retail investors. Raising the threshold is the simplest and most realistic compromise.

2) Start with domestic exchanges

Given practical limitations, enforcement will likely begin with transactions on domestically regulated exchanges, where data is already available. Overseas exchanges and self-custodied wallets are more difficult to track and will likely be incorporated gradually.

Implementation may be immediate, but enforcement will be phased.

3) Soft enforcement in the early stage

Even if the system starts in 2027, early enforcement is likely to focus on compliance and data accumulation rather than strict penalties. More complex transaction types will be addressed over time as rules and infrastructure mature.

Legal implementation and strict enforcement are not the same.

Conclusion

January 1, 2027 remains a valid timeline. However, it no longer implies implementation in its original form.

Since March 2026, political actors have reintroduced the issue, shifting the focus from whether taxation will happen to how it will be structured. While the ruling party raises concerns around fairness and feasibility, the opposition has not fully aligned on repeal, and administrative institutions continue preparing for implementation.

Given this combination, the most likely outcome is not full repeal, but modified implementation.

For investors, the key variables are threefold: the level of the exemption threshold, the order in which different transaction types are taxed, and the intensity of early enforcement. Ultimately, the most impactful factor for the market will not be whether taxation occurs, but how it is designed.

At this stage, Korea appears to be moving not toward abandoning taxation, but toward refining it and integrating it into the formal financial system.

Disclaimer

This material is provided for informational and research purposes only and does not constitute investment advice, nor is it intended to recommend the purchase, sale, or holding of any asset (including equities or tokens), or to replace independent investment judgment.

All views and analyses expressed herein are based on publicly available information and reasonable assumptions as of the time of writing, and are subject to change depending on market conditions, policy developments, or regulatory changes.

This research has been prepared independently and without any financial compensation, sponsorship, or incentives from any of the projects or their affiliated parties mentioned. However, the author or affiliated organization may have had prior commercial relationships with such projects, and potential conflicts of interest may exist. All opinions and interpretations presented in this material reflect the independent judgment of the author.

The final responsibility for any investment decisions rests solely with the reader. The author assumes no legal liability for any outcomes resulting from reliance on this content.

Terms of Use

Exilist permits the fair use of its research materials for non-commercial and informational purposes, provided that the original meaning and analytical context are preserved.

Proper attribution to Exilist is required when referencing or citing this publication.

Any form of republication, translation, modification, commercial distribution, or derivative use of this material, in whole or in part, requires prior written consent from Exilist.

Unauthorized commercial use, misrepresentation of analytical conclusions, or distribution without proper attribution may result in legal action.