Tokenized Equities: Where the Real Battle Lies

Ondo GM, xStocks, and Robinhood — Structures, Trade-offs, and Value Capture Paths

Executive Summary

The competitive landscape of tokenized equities is not determined by who lists the most assets first. Rather, it is defined by who can most convincingly integrate rights structures, real-world asset backing, clearing and settlement infrastructure, and onchain liquidity into a coherent system.

From this perspective, Ondo GM demonstrates strength in collateralization, verification, and multi-chain distribution. Robinhood, on the other hand, is strongest in regulated distribution through a retail-native application layer. However, the largest long-term upside likely resides with xStocks. This is because xStocks sits closest to the intersection between permissionless onchain liquidity and the onshore tokenization infrastructure currently being developed by Nasdaq.

From an investor standpoint, a more important point is that these three platforms do not implement the same type of “tokenized stock.” Ondo GM is structured as a debt security in the form of a structured note, xStocks operates as an asset-backed tracker certificate, and Robinhood offers an OTC derivative contract represented through tokens. As a result, the growth of tokenized equities should not be assumed to benefit all three equally. The direction of market expansion—whether toward DeFi integration, regulated brokerage expansion, or onshore rights-equivalent systems connected to DTCC/DTC—will determine where value ultimately accrues.

In conclusion, the policy and infrastructure trajectory of 2026 is moving away from pure permissionless expansion and toward the question of how permissionless systems can connect with onshore, rights-equivalent frameworks. In this context, xStocks represents the most aggressive upside option, Ondo GM offers stronger current scale and defensiveness, and Robinhood should be understood less as onchain financial infrastructure and more as a brokerage model that absorbs tokenization into a retail application.

Introduction

Tokenized equities appear to be a single asset class, but in reality they encompass multiple distinct legal formats under the same label. Some are structured as debt securities in the form of structured notes, others are certificates backed by real equities, and still others are derivative contracts distributed through brokerage applications. While they may all appear as “stock tokens” on the surface, their legal substance and rights structures are fundamentally different.

Therefore, similarity in price behavior should not be mistaken for equivalence. Exposure to the same underlying equity—such as Apple—can carry entirely different implications depending on whether the asset represents direct ownership, a tracker certificate, or a contractual claim against a platform. What matters is not which platform is more well-known, but what the token legally represents, what it is backed by, what rights it confers, and who ultimately controls it.

Competition in tokenized equity infrastructure cannot be reduced to a purely technological race. On one side, there is a push toward permissionless global distribution and DeFi integration. On the other, the United States is advancing an onshore model that preserves existing financial infrastructure while incorporating token formats. Robinhood operates between these approaches, emphasizing brokerage UX to translate tokenization into a consumer-facing financial product. The current market is not converging toward a single winner, but rather reflects the coexistence of three competing design philosophies.

Permissionless systems, in simple terms, allow assets to move freely and be traded by anyone with a wallet. Onshore systems, by contrast, operate within regulatory jurisdictions such as the United States. Rights-equivalent structures imply that tokenized assets must preserve the same rights as traditional equities, including dividends, voting, shareholder registry linkage, and corporate action handling.

In this sense, the direction being pursued by U.S. regulatory frameworks—combining permissionless mobility with onshore regulatory compliance and full rights equivalence—represents a highly complex objective. At present, most tokenized equity infrastructures do not simultaneously satisfy all three conditions.

Debt-based tokenized equities, such as Ondo GM, represent obligations by the issuer to deliver returns linked to underlying assets. Rather than granting ownership, they promise to replicate economic exposure. In such structures, tracking accuracy is important, but so are the safety of the issuance structure and the sufficiency of collateral.

Asset-backed tracker models, such as xStocks, are not synthetic exposures but certificates backed 1:1 by real equities. While users do not hold shares directly in their own name, the underlying assets are held in custody, and the certificate reflects their value with a priority claim structure. This design sacrifices certain shareholder rights but enables greater transferability and usability in onchain environments.

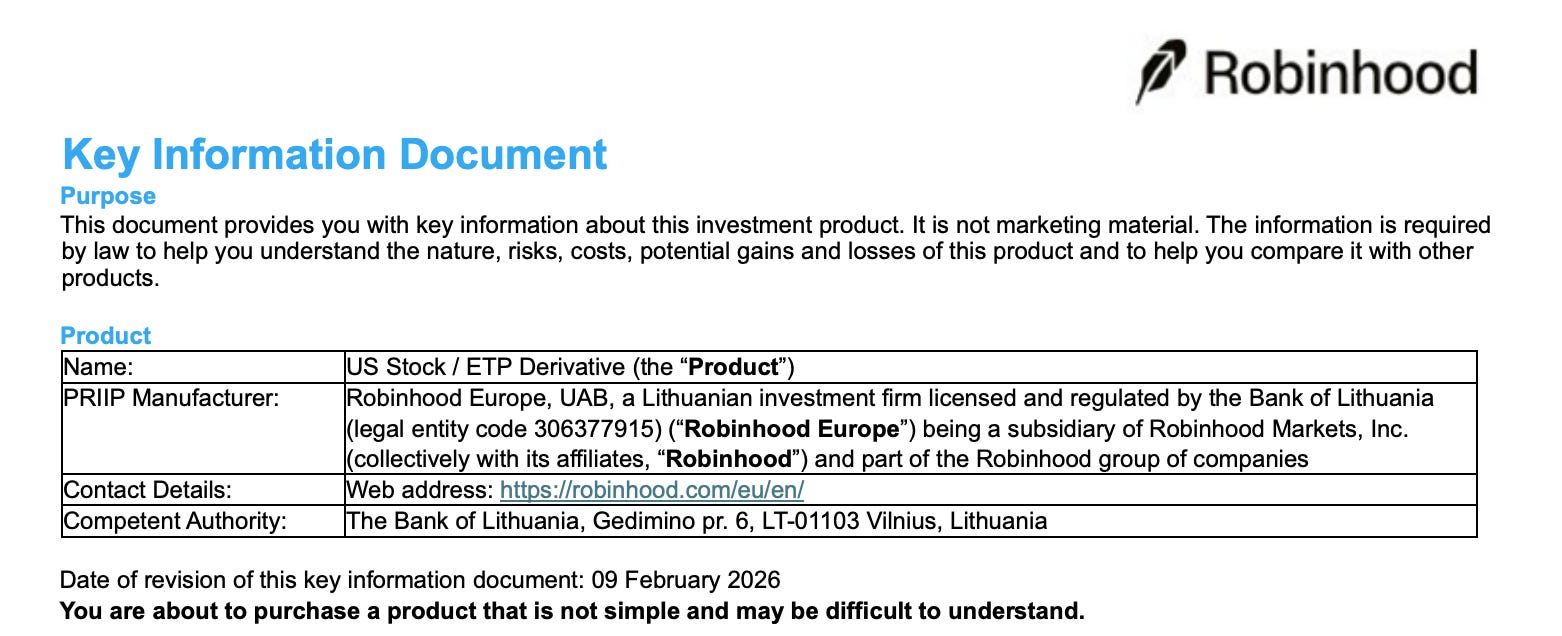

Derivative-based tokenized equities, such as those offered by Robinhood, represent contractual exposure derived from underlying assets. Users do not own shares but instead hold rights under an OTC derivative contract with the platform. In this case, the primary risk is not just the underlying equity but also counterparty risk.

Robinhood’s model can also be interpreted as a brokerage framework. Rather than treating tokenized equities as onchain assets, it packages them as consumer financial products within an application. While this enables familiar UX and rapid distribution, it limits composability and self-custody.

1. The Real Comparison Is Not Tokens, But Product Formats

The ambiguity of the term “tokenized equities” is the first critical issue. Under the same label, an asset may legally be a debt security, a tracker certificate, or a derivative contract. This distinction is not merely semantic. It determines how dividends are distributed, whether voting rights exist, whether physical redemption is possible, who holds priority in bankruptcy, and how regulators classify the instrument.

For investors, the key question is not whether an asset behaves like a stock, but what rights are being forfeited in exchange for convenience.

The first point of differentiation is shareholder rights. Ondo GM provides economic exposure but does not grant voting or information rights. xStocks also does not provide direct ownership of underlying shares and does not grant voting or cash dividend claims. Robinhood is even more explicit: users hold contractual rights against Robinhood Europe rather than equity ownership. While none of the three platforms provides direct ownership of shares, the degree of separation from underlying assets differs significantly. Ondo GM and xStocks maintain stronger links to backing assets, whereas Robinhood operates primarily through contractual exposure.

2. Ondo GM: A Structured Note Model Anchored in Collateral and Verification

However, this model comes with trade-offs. Reliance on Reg S exemptions introduces structural limitations on U.S. participation. Dividend flows are subject to withholding tax, which can reduce net returns for token holders. Costs are not always explicit, but are embedded within bid-ask spreads and execution pricing.

Ultimately, Ondo GM represents a structure that prioritizes strong collateral narratives and global distribution, at the expense of shareholder rights, onshore accessibility, and certain aspects of net yield.

3. xStocks: From Certificate-Based Trackers to an Onchain Liquidity Layer

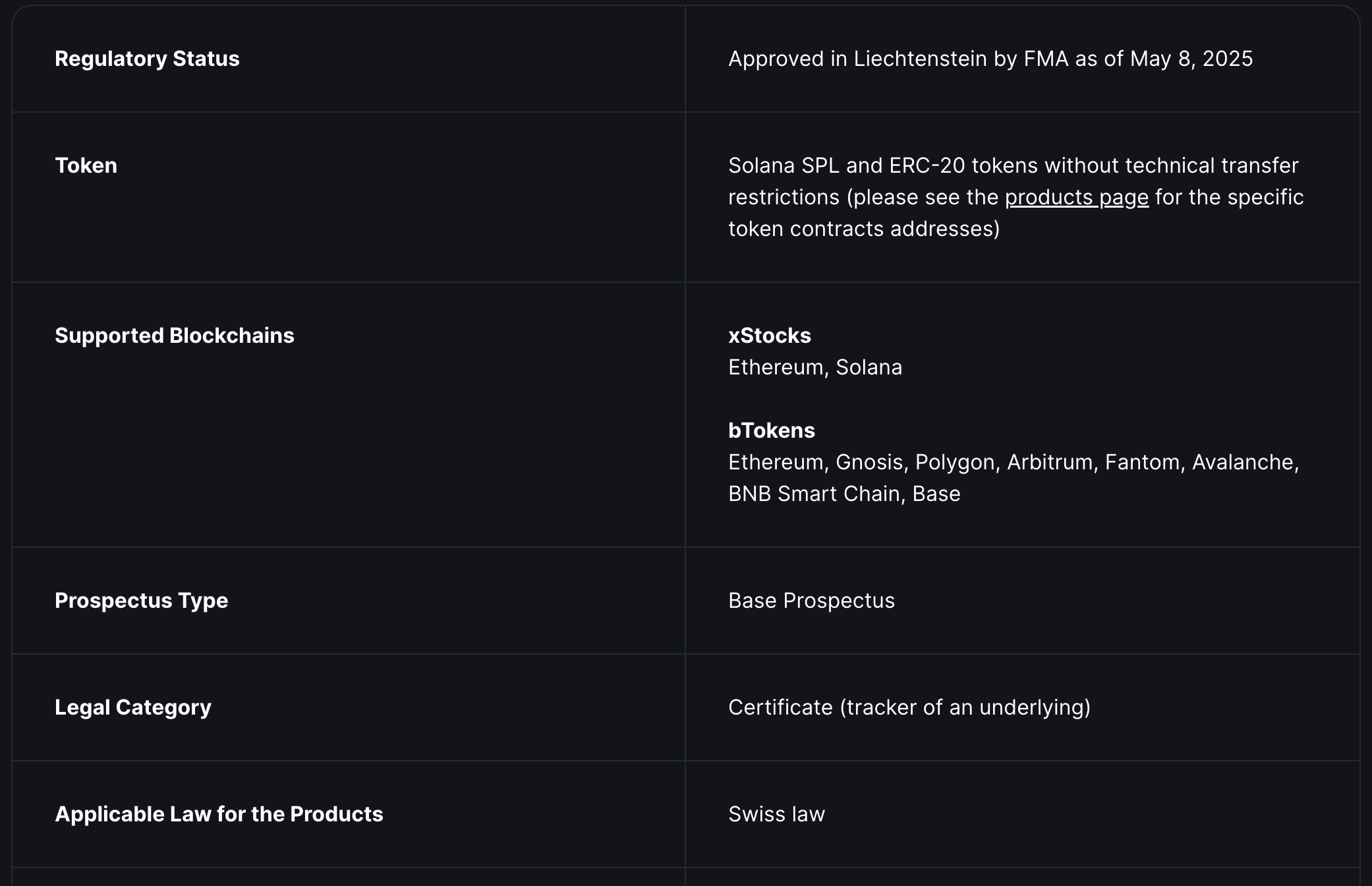

xStocks differs from exchange-issued token models by separating issuance from distribution. The underlying instrument is a certificate issued by a dedicated entity, while crypto platforms provide trading, distribution, and custody interfaces. The legal structure is defined under European prospectus frameworks, with disclosures covering issuer structure, jurisdiction, service providers, and security agents. Supported token standards include Solana SPL and ERC-20.

One of the key differentiators lies in how economic rights are transmitted. Rather than distributing cash dividends, xStocks reinvests them into the token structure, adjusting its multiplier accordingly. This design allows dividend effects to be reflected in token value rather than cash flow, making it more compatible with onchain financial use cases such as collateralization, lending, and liquidity provision.

A critical development occurred when Kraken acquired Backed Finance, the issuer behind xStocks. This brings issuance, distribution, and liquidity layers into closer alignment under a single ecosystem. The significance lies not only in scale, but in coordination. When these layers are unified, fee structures, spread policies, incentives, and infrastructure development can be aligned into a single strategic direction.

As a result, xStocks is evolving beyond a standalone product into a potential onchain equity liquidity network.

4. Robinhood: Tokenization as an Extension of Brokerage Products

Robinhood’s tokenized equities have the clearest legal definition among the three. They are OTC derivative contracts provided by Robinhood Europe UAB. Users do not own shares or certificates, but hold contractual exposure to price movements.

The token functions primarily as a representation layer rather than the asset itself. While each token corresponds to an underlying share or unit in price terms, it does not grant redemption rights or shareholder privileges.

The strength of this model lies in distribution. Robinhood offers over 200 tokenized equities and ETFs to European users, initially using Arbitrum L2, with plans to expand into its own infrastructure. The focus is not on building DeFi-native financial primitives, but on delivering a seamless and familiar user experience.

However, the limitations are equally clear. Counterparty risk is concentrated in a single entity, investor protections are limited, and the product carries a high risk classification under European standards. While effective as a distribution model, it lacks the composability and self-custody features that characterize onchain financial assets.

5. Scale and Chain Distribution: Where Is Real Usage Happening?

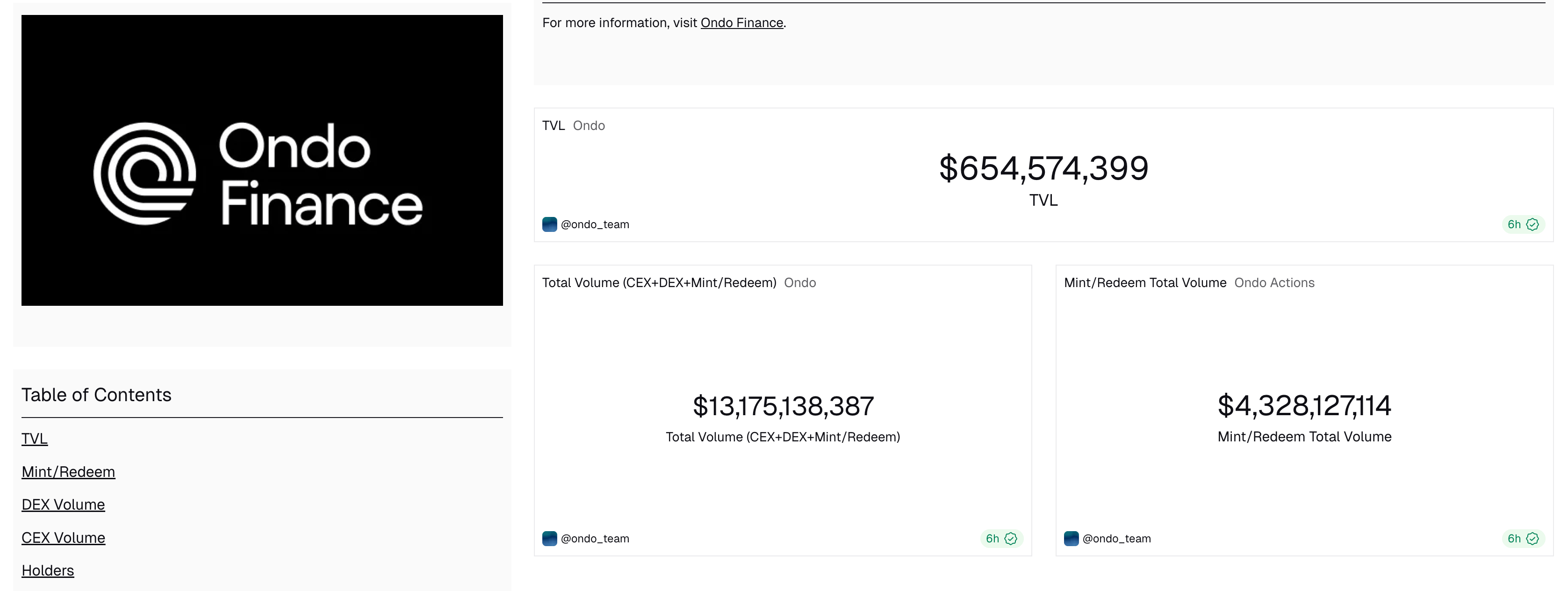

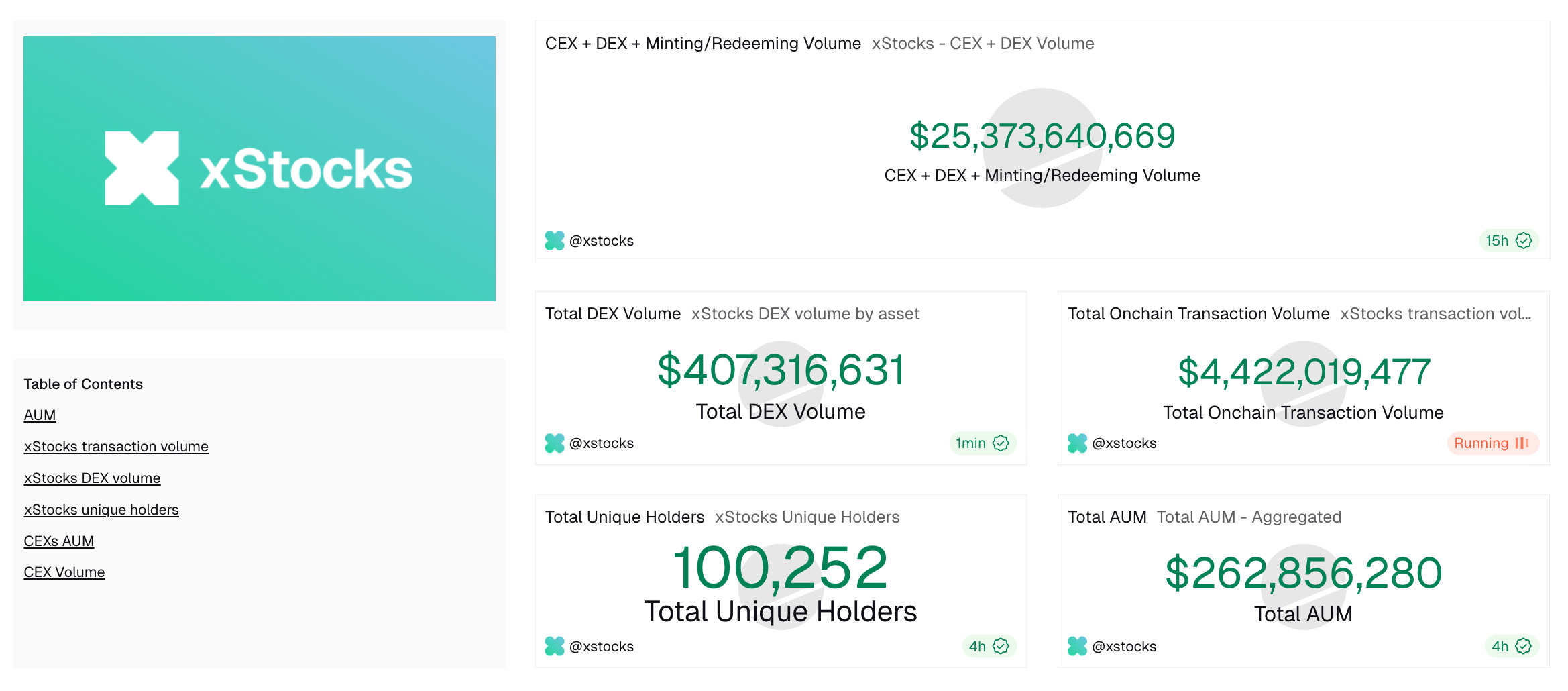

From an onchain perspective, the most objective measure of scale is total value locked (TVL). Ondo GM currently stands at approximately $654 million, while xStocks is at around $262 million.

Ondo GM’s liquidity is distributed across multiple chains, with approximately $419 million on Ethereum, $216 million on BNB Chain, and $17.2 million on Solana. In contrast, xStocks is almost entirely concentrated on Solana.

Robinhood, by comparison, does not operate within public DeFi TVL frameworks. Instead, its scale is better understood through product distribution, user base, and geographic reach. Based on available reporting, it serves approximately 150,000 users across around 30 countries.

These figures reveal more than just current market share. Ondo GM reflects strong distribution across EVM ecosystems and alignment with institutional custody infrastructure. xStocks, on the other hand, reflects concentrated usage within a high-performance, low-cost environment, enabling dense onchain activity. Ondo GM is therefore stronger in multi-chain reach and defensiveness, while xStocks is stronger in the intensity of onchain usability.

Robinhood operates outside of this comparison. Its competitive axis is not TVL, but rather user conversion, engagement, and the ability to absorb tokenized exposure into a brokerage experience.

Differences in token standards and transferability further reinforce this divergence. Ondo GM maintains consistent economic exposure across chains, though representation may vary by network. xStocks explicitly adopts transferable token standards such as SPL and ERC-20, with minimal restrictions, reflecting a design philosophy oriented toward permissionless movement and DeFi integration. Robinhood, even when using blockchain infrastructure, ultimately operates through application-level contracts, where positions are opened and closed within the platform.

In this sense, Ondo GM and xStocks are fundamentally onchain assets, while Robinhood represents a brokerage product with an onchain representation layer. Even within the same “tokenized equity” category, composability differs significantly.

6. Revenue Structures and Fee Models: Where Does the Platform Capture Value?

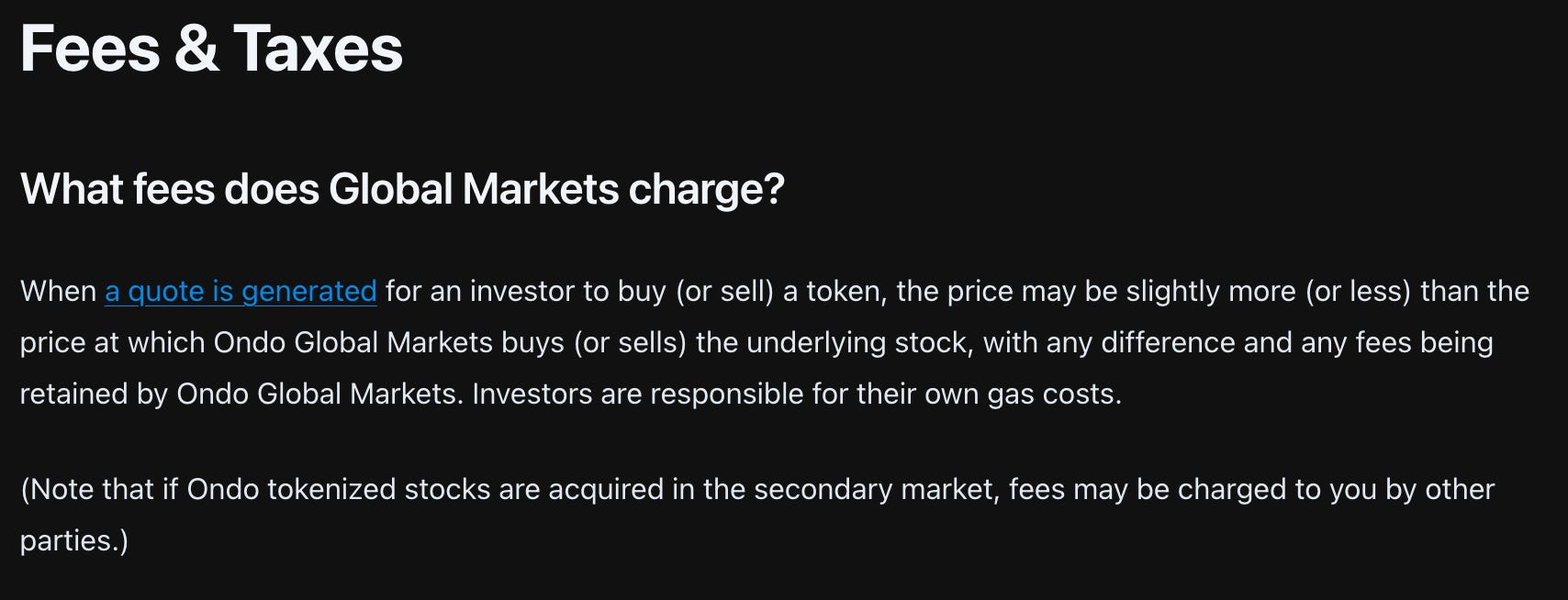

Ondo GM does not charge explicit minting or redemption fees, but its economics are embedded within pricing spreads. The execution price may deviate from the underlying asset price, with the difference captured by the platform.

For example, if the reference price of an underlying equity is $100, but Ondo GM quotes a purchase price of $100.40, the investor effectively pays a 0.40% implicit cost. While no explicit fee is displayed, the spread functions as a pricing mechanism through which value is captured.

In Ondo GM’s structure, price appreciation and reinvested dividend effects accrue to token holders, while spread-based revenue accrues to the platform.

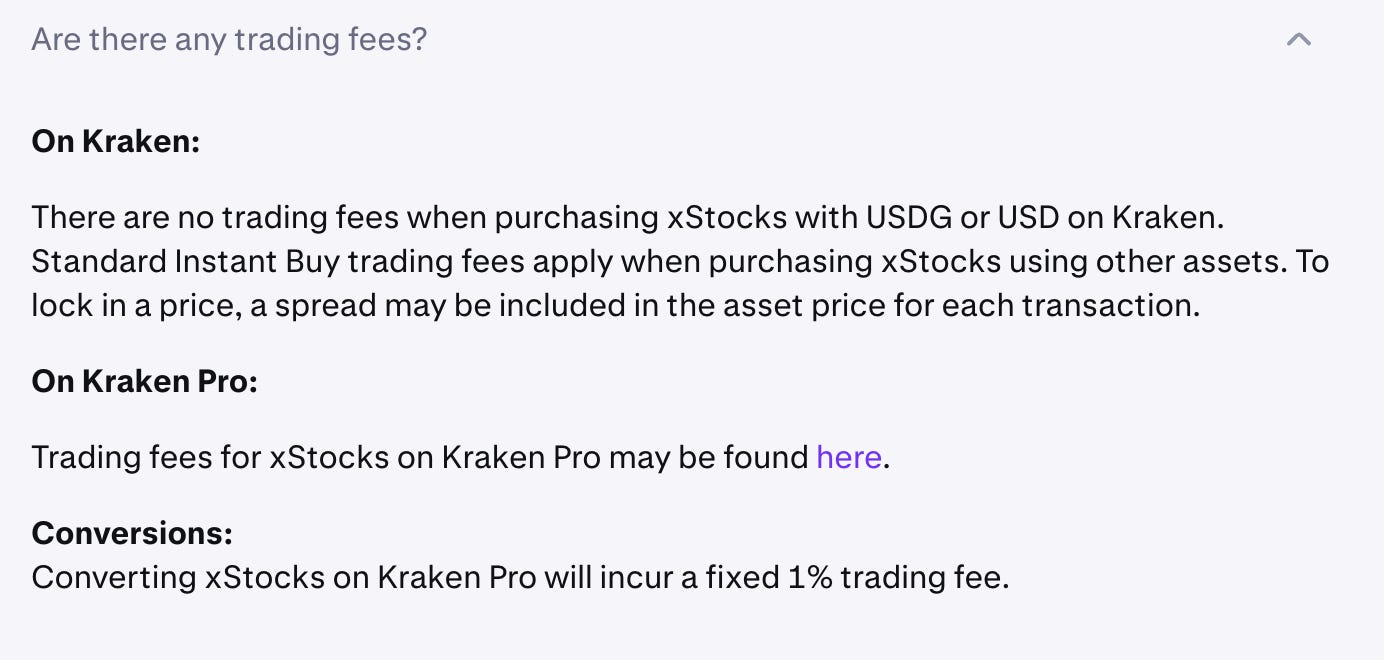

xStocks operates a more layered model. Within Kraken’s exchange environment, certain trading pairs such as USD-based pairs may be offered with zero trading fees. However, standard fees and spreads apply when using other assets. Additional layers include conversion fees, such as the 1% fee in Kraken Pro’s Convert function, as well as embedded product-level fees defined in the prospectus.

Beyond centralized exchange activity, xStocks also interacts with external infrastructure such as Bybit, Raydium, Orca, and Phantom Wallet, where additional fees are determined by those platforms. While direct transaction fees may not always be explicit, xStocks incorporates issuer-level and product-level fee structures.

Importantly, xStocks integrates these costs into a broader incentive system. The introduction of programs such as xPoints reflects an attempt to offset friction through ecosystem rewards, effectively redistributing part of the economic capture back into liquidity growth.

Robinhood presents its fee structure more directly. Entry and exit fees are capped at approximately 0.10%, and foreign exchange conversion is embedded in the transaction process. While external messaging may emphasize commission-free trading, the product documentation indicates that revenue is primarily generated through derivative pricing, FX spreads, and platform-level margins.

Dividends are not received as shareholder distributions, but rather reflected through contractual adjustments or cash flows within the derivative framework. This reinforces the distinction: Ondo GM operates as a structured product, xStocks as a liquidity network with layered monetization, and Robinhood as a brokerage-driven derivative platform.

7. What Regulation Actually Favors: The U.S. Perspective on Tokenized Equities

As of March 2026, regulatory signals from the SEC and CFTC indicate a consistent principle: digital assets may be classified more flexibly, but digital securities remain securities. Representing a stock as a token does not reduce regulatory requirements. Instead, it introduces additional challenges in maintaining equivalence.

The key requirement is ensuring identical rights, transparency, market surveillance, and settlement processes. Permissionless distribution alone is insufficient for integration into onshore financial systems.

This is where broader legislative developments become relevant. The GENIUS Act introduces stricter requirements for stablecoin reserves and disclosures, effectively aligning onchain payment rails with regulated financial infrastructure. This matters because tokenized equities cannot operate independently of their settlement layer. Dividend distributions, corporate actions, and payments all depend on compliant financial rails.

The CLARITY Act, focused on market structure, further influences incentive design, including restrictions around stablecoin-based rewards. Together, these frameworks indicate that the future of tokenized equities will be shaped not only by token design, but by the integration of regulated payment systems.

Under these conditions, the regulatory preference becomes clearer. Systems that preserve rights equivalence, maintain standardized identifiers such as CUSIPs, integrate with existing clearing infrastructure like DTCC/DTC, and allow controlled transfer through approved wallets are more likely to align with onshore requirements.

From this perspective, Ondo GM and xStocks, despite strong asset backing, remain primarily offshore or global distribution models. Robinhood operates as a brokerage-layer wrapper. None fully match the onshore, rights-equivalent model currently favored by U.S. infrastructure.

The key question is not whether these platforms fit today’s model, but which one can evolve toward it.

8. The Nasdaq–DTC Pilot: Not Tokenization of Markets, but Tokenization of Format

The recent Nasdaq rule change approved by the SEC does not represent a shift toward fully onchain markets. In fact, it suggests the opposite.

Tokenized equities within this framework must remain within the DTC system, maintain identical rights and identifiers as traditional equities, and settle through existing clearing infrastructure. This is not an attempt to replace the system, but to extend it by introducing token formats.

In other words, the U.S. approach is not to build a parallel market, but to embed tokenization within the existing one.

For investors, the key question becomes straightforward: which platform is structurally closest to this model?

Robinhood, as a European derivative-based platform, is structurally distant. Ondo GM, while strong in collateralization, does not provide rights equivalence due to its structured note format.

However, Ondo should not be viewed solely as an offshore player. Through its acquisition of Oasis Pro, it has secured key components of U.S. infrastructure, including a registered broker-dealer, an alternative trading system (ATS), and transfer agent capabilities. Its confidential SEC filing in early 2026 further suggests an intention to align with onshore frameworks.

xStocks, while not yet rights-equivalent, combines real asset backing with permissionless distribution infrastructure. Importantly, Nasdaq has explicitly referenced xStocks as a potential counterparty in its design framework. Nasdaq describes its tokenized equity model as preserving issuer rights while aligning legal and operational structures with traditional equities.

While it is too early to conclude that xStocks represents the final onshore solution, it is currently one of the closest candidates positioned at this intersection.

9. Nasdaq–Payward (Kraken)–xStocks: The Most Critical Connection

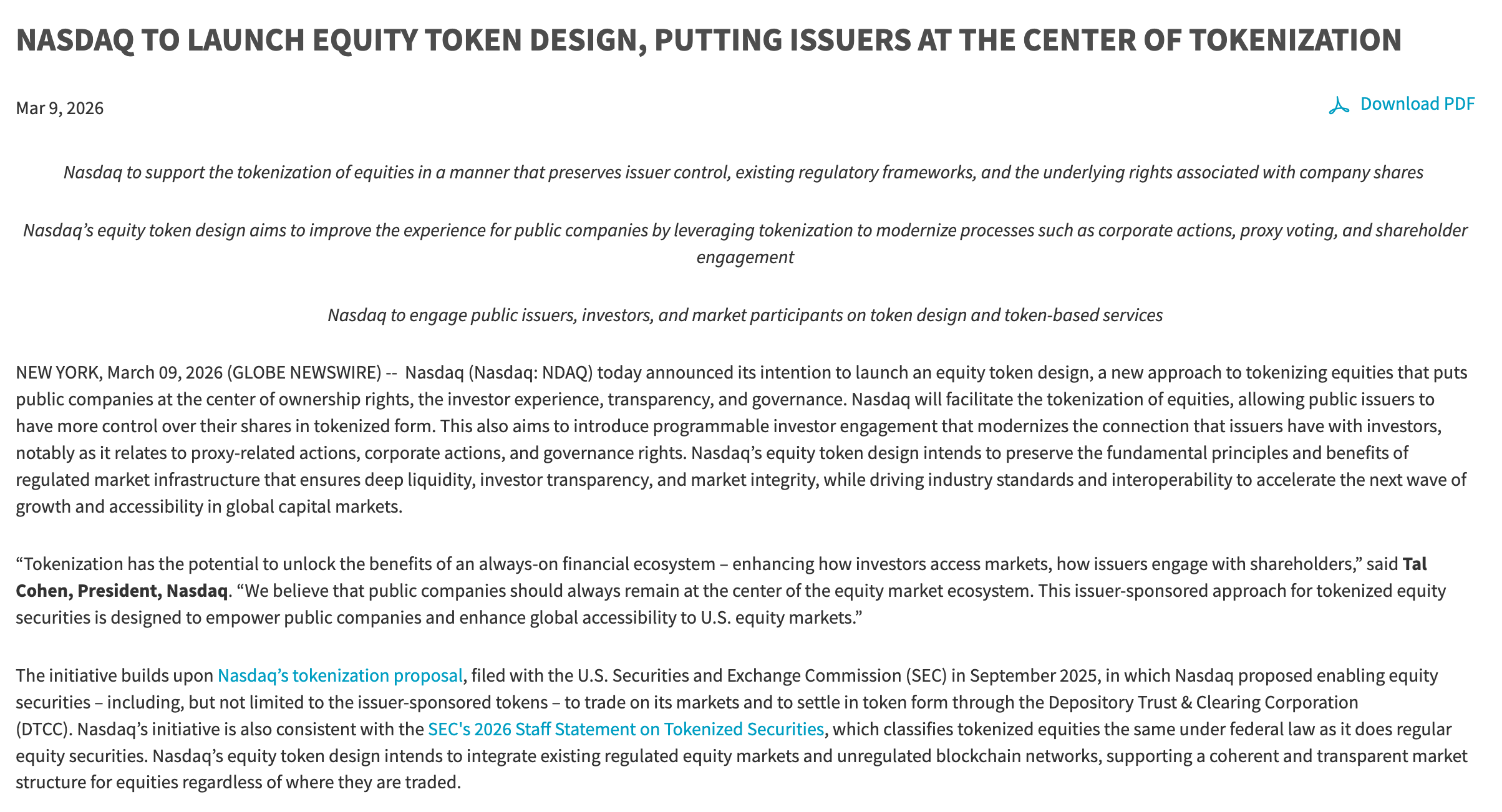

The most important development in this landscape is Nasdaq’s issuer-sponsored equity token design. This model aims to link official shareholder registries with onchain records, ensuring that token transfers correspond directly to underlying equity ownership.

Within this framework, Nasdaq explicitly references collaboration with Payward, Kraken’s parent company, and xStocks infrastructure to build an “equities transformation gateway” connecting permissioned and permissionless markets. The target timeline is the first half of 2027.

This represents a fundamental shift. Until now, tokenized equities have been divided between offshore DeFi-oriented systems and regulated brokerage models. Nasdaq introduces a third path: maintaining traditional market structures while integrating onchain transferability.

In this model, xStocks is not simply a product, but a potential bridge layer connecting two previously separate systems.

From an investment perspective, this is critical. The long-term winner in tokenized equities will not be determined solely by trading volume. It will depend on the ability to integrate onshore regulated assets, permissionless liquidity, stablecoin settlement, and legal alignment with issuance and transfer systems.

xStocks is not yet a complete solution, but it is positioned at the intersection of these components.

Ondo GM may currently offer stronger scale and defensiveness, but its connection to onshore infrastructure is less explicitly defined. While Ondo is actively building toward this direction, the xStocks–Nasdaq connection is currently more direct and formally articulated.

10. What the DTC Pilot Implies About the Next Generation of Platforms

The DTC no-action framework suggests that future platforms may be more conservative than expected.

Transfers may be restricted to approved wallets. Initially, tokens may not carry collateral or settlement value. Corporate actions may eventually be processed through stablecoins or tokenized deposits.

This implies that the first generation of onshore tokenized equity platforms will not be fully permissionless. Instead, they will likely adopt a partially open model that balances accessibility with regulatory compliance.

This shifts the competitive landscape. Ondo GM and xStocks are strong because they address current onchain user demand. Robinhood is relevant because it captures retail distribution.

However, the next phase of infrastructure prioritizes rights equivalence, controlled transfer, corporate action handling, and integration with existing systems. This creates a new category where bridge-layer participants become increasingly valuable.

11. NYSE–Securitize and Alternative Launch Pathways

While Nasdaq’s approach focuses on integrating tokenization into existing infrastructure, the NYSE–Securitize partnership represents a different path.

This model explores the possibility of dedicated digital venues for tokenized securities, with Securitize acting as a blockchain-based transfer agent and NYSE contributing regulatory and operational frameworks. It also introduces the possibility of 24/7 trading and stablecoin-based instant settlement.

These two approaches represent parallel paths. One extends the existing system through token formats, while the other builds new infrastructure for digital securities.

As the market evolves, both paths are likely to coexist. In this context, platforms like xStocks may extend beyond DeFi-native environments and connect with both models. Ondo GM is more likely to remain a strong offshore distribution hub, while Robinhood continues to focus on consumer-facing expansion.

Conclusion

Comparing these three platforms as direct competitors oversimplifies the landscape. While they appear to operate within the same category, they address fundamentally different problems.

Ondo GM focuses on trust and verification in offshore tokenized equities. Robinhood translates tokenization into a consumer-friendly brokerage experience. xStocks attempts to integrate real asset backing, onchain liquidity, exchange distribution, and potential connections to onshore infrastructure.

From an investment perspective, the framework becomes clearer. Ondo GM offers strong current defensiveness and scale. Robinhood dominates retail distribution. However, xStocks presents the most asymmetric upside, particularly if tokenized equities evolve toward a model that connects permissionless liquidity with onshore, rights-equivalent infrastructure.

That said, this upside is contingent on execution. Nasdaq’s framework remains in development, with a target timeline of 2027. The DTC pilot remains conservative in scope. As a result, xStocks carries both higher upside and higher implementation risk.

Ultimately, the defining question is not who tokenizes equities first, but who successfully integrates regulatory compliance, real asset backing, settlement rails, and onchain liquidity into a unified system.

Disclaimer

This material is provided for informational and research purposes only and does not constitute investment advice, nor is it intended to recommend the purchase, sale, or holding of any asset (including equities or tokens), or to replace independent investment judgment.

All views and analyses expressed herein are based on publicly available information and reasonable assumptions as of the time of writing, and are subject to change depending on market conditions, policy developments, or regulatory changes.

This research has been prepared independently and without any financial compensation, sponsorship, or incentives from any of the projects or their affiliated parties mentioned. However, the author or affiliated organization may have had prior commercial relationships with such projects, and potential conflicts of interest may exist. All opinions and interpretations presented in this material reflect the independent judgment of the author.

The final responsibility for any investment decisions rests solely with the reader. The author assumes no legal liability for any outcomes resulting from reliance on this content.

Terms of Use

Exilist permits the fair use of its research materials for non-commercial and informational purposes, provided that the original meaning and analytical context are preserved.

Proper attribution to Exilist is required when referencing or citing this publication.

Any form of republication, translation, modification, commercial distribution, or derivative use of this material, in whole or in part, requires prior written consent from Exilist.

Unauthorized commercial use, misrepresentation of analytical conclusions, or distribution without proper attribution may result in legal action.