KOSPI 8,000 Doesn’t Kill the Altseason. It May Trigger It.

Why Korea’s AI Semiconductor Rally Could Become the Starting Point for KRW Altcoin Liquidity

Introduction

As of May 2026, the center of gravity in Korean markets is no longer crypto. It is equities.

The KOSPI is approaching 8,000 for the first time in history, while Samsung Electronics and SK Hynix are leading one of the strongest AI semiconductor rallies Korea has seen in years. What initially looked like a simple thematic trade has evolved into something larger: a retail-accessible narrative around industrial growth that Korean investors can directly understand and emotionally participate in.

Generative AI adoption, accelerating data center investment, and rising HBM demand have all translated into stronger earnings expectations for Korean semiconductor leaders. As a result, Korean retail liquidity has aggressively rotated back into equities.

At first glance, this appears bearish for crypto.

Domestic crypto exchange balances and trading activity have fallen significantly from previous cycle highs. Bitcoin has reclaimed $80,000, yet the retail-driven altcoin mania Korean traders continue waiting for has still not arrived.

However, this report argues that many investors may be interpreting the current setup incorrectly.

Liquidity has not disappeared from crypto markets.

It is simply parked elsewhere for now.

Korean retail investors are not avoiding risk assets. On the contrary, they are rediscovering risk appetite through AI semiconductor equities, KOSPI momentum, and thematic growth stocks. The key difference is that the destination of capital is currently equities rather than crypto.

The central question of this report is therefore straightforward:

Can capital that flowed into KOSPI large caps, KOSDAQ themes, and AI semiconductor momentum eventually rotate back into KRW-denominated altcoin markets?

Meanwhile, the first stage of crypto recovery is already underway.

Bitcoin has reclaimed $80,000, global crypto market capitalization remains above $2.7 trillion, and ETF inflows have resumed. Institutional participation continues expanding through regulated infrastructure.

Still, this recovery remains heavily Bitcoin-centric. Altseason indicators remain below historical thresholds, while domestic altcoin trading activity remains far below previous speculative peaks.

Nevertheless, multiple structural conditions are beginning to align simultaneously.

Institutional and ETF capital has already re-entered crypto through Bitcoin.

Stablecoin supply and KRW exchange deposits suggest sidelined liquidity still exists both inside and outside crypto markets.

U.S. regulation is increasingly moving toward formal integration of stablecoins and digital asset market structure into traditional finance.

Most importantly, KOSPI 8,000 itself signals the return of Korean retail risk appetite.

In the short term, this absorbs liquidity away from crypto. But in the medium term, it may become the starting point for rotation into higher-beta assets.

This matters because Korea occupies a uniquely important position within altcoin spot markets.

Compared to most global markets, Korea structurally favors altcoins over Bitcoin and operates through highly concentrated KRW-based spot trading infrastructure. Korean retail investors generate exceptionally high turnover in altcoin trading, particularly through Upbit and Bithumb.

As a result, if Korean retail risk appetite rotates from equities back into KRW altcoin markets, price elasticity across altcoins could expand dramatically.

The base-case scenario outlined in this report is relatively simple:

BTC leadership → AI semiconductor rally → profit-taking and corrections in large-cap equities → search for higher-beta recovery trades → recovery in large-cap altcoins → expansion of AI/RWA/tokenized equity narratives → re-ignition of KRW altcoin markets → speculative rotation into smaller and lower-liquidity altcoins

The conditions for a full altseason are not yet complete.

But the liquidity, psychology, regulation, and narrative conditions required for one are accumulating rapidly.

The current KOSPI rally is not necessarily the opposite of an altseason.

It may actually be the earliest signal that Korean retail risk appetite is returning.

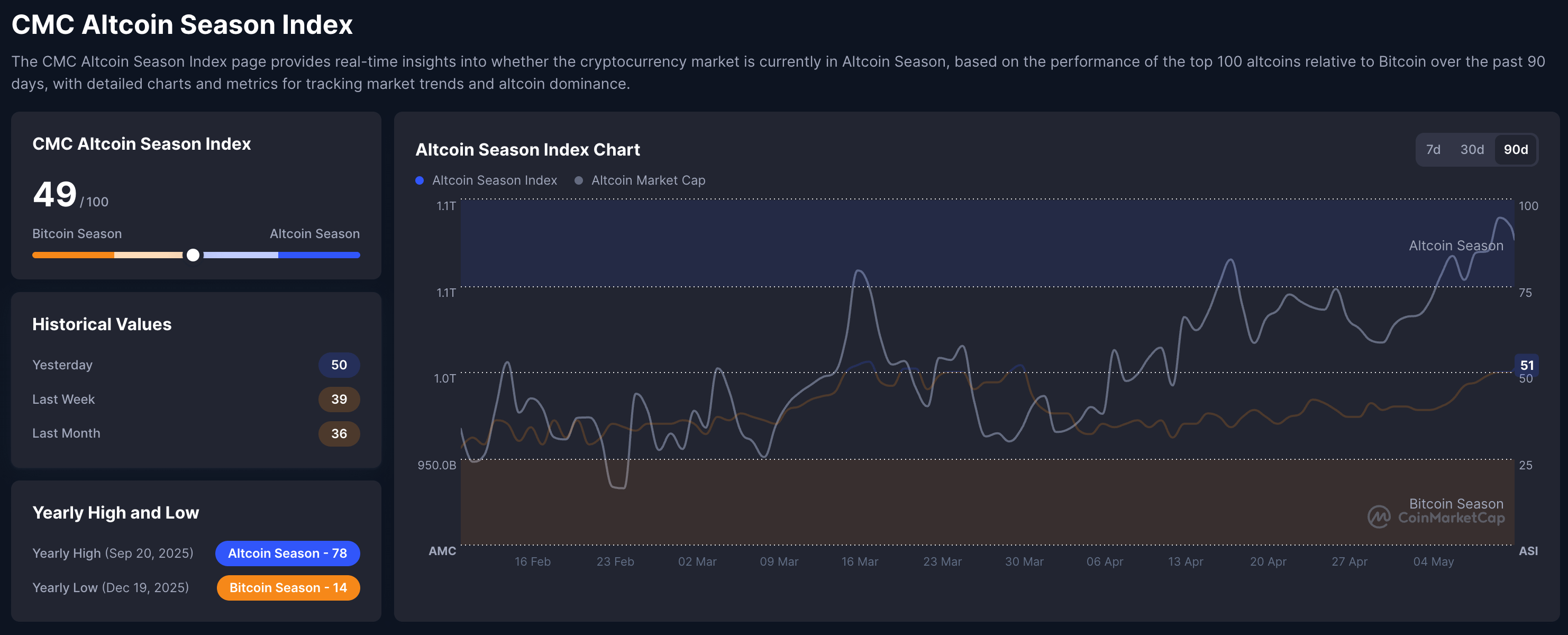

1. Bitcoin Reclaimed $80,000. But This Is Still Not an Altseason.

In early May 2026, Bitcoin reclaimed the $80,000 level once again.

According to CoinMarketCap data as of May 12, Bitcoin traded around $81,000 while global crypto market capitalization remained near $2.7 trillion. BTC dominance remained near 60%, confirming that the market is still decisively Bitcoin-centric.

CoinMarketCap’s Altcoin Season Index compares the 90-day performance of the top 100 cryptocurrencies against Bitcoin. Historically, readings above 75 are considered indicative of an altseason. As of early May, the index remained near 50.

BlockchainCenter’s altseason index applies a similar framework, requiring 75% of the top 50 assets to outperform Bitcoin over a 90-day period. Recent readings remained near 35.

By historical standards, this is still far from a broad altcoin outperformance cycle.

However, interpreting these indicators purely as bearish signals would be misleading.

Altseason indicators are inherently lagging metrics.

By the time such indicators exceed 75, a large portion of the strongest altcoin performance has often already occurred. Historically, the most asymmetric returns frequently emerge before the indicator fully confirms an altseason.

Therefore, low altseason readings today do not necessarily indicate that altseason will fail to arrive.

Rather, they suggest that liquidity remains concentrated in Bitcoin for now.

This sequence is natural.

Institutional capital almost always enters Bitcoin first. Bitcoin possesses the deepest liquidity, the longest market history, and the strongest ETF and custody infrastructure. BlackRock, Fidelity, and other major asset managers have primarily opened institutional access through spot Bitcoin ETFs.

As a result, Bitcoin dominance does not contradict the possibility of a future altseason.

Instead, it may represent the first stage preceding one.

The more important question is not whether this is already an altseason.

The real question is:

Under what conditions does liquidity concentrated in Bitcoin begin rotating into altcoins?

2. Korea’s Crypto Market Is Not Dead. It Is Waiting.

On the surface, Korea’s domestic crypto market appears weak.

According to Bank of Korea data cited by local media, crypto asset holdings across Korea’s five major exchanges fell from KRW 121.8 trillion at the end of January 2025 to KRW 60.6 trillion by the end of February 2026.

Average daily trading volume also collapsed from KRW 17.1 trillion in December 2024 to KRW 4.5 trillion in February 2026.

At face value, these figures suggest a market in deep decline.

However, another part of the same dataset deserves far greater attention.

Stablecoin balances across Korea’s five major exchanges increased from KRW 88.5 billion in July 2024 to KRW 872.3 billion by December 2025, before stabilizing near KRW 607.1 billion at the end of February 2026.

Compared to January 2025, stablecoin balances still remained roughly 2.2x higher.

In other words, speculative positioning declined, but sidelined liquidity remained inside the system.

The Financial Services Commission (FSC) and FIU’s second-half 2025 survey points in the same direction.

While trading activity weakened, KRW exchange deposits increased.

According to official figures across 27 registered Korean virtual asset service providers, KRW exchange deposits reached approximately KRW 8.1 trillion by the end of 2025, while the number of active trading accounts rose to roughly 11.13 million.

This distinction matters.

Trading volume measures current market heat.

Deposits and stablecoin balances measure re-entry potential.

Korea’s crypto market has cooled in terms of active speculation, but liquidity remains inside the system.

This resembles waiting behavior rather than full market abandonment.

Altseasons rarely begin when speculative activity is already overheated.

They often begin when positioning has cooled while liquidity never fully left.

The current Korean crypto market increasingly resembles that setup.

3. Korea Is One of the Most Important Variables in Altcoin Spot Markets

Korea matters more in altcoins than in Bitcoin.

Bitcoin pricing is primarily driven by ETF flows, institutional capital, and global derivatives markets. Altcoins, especially mid- and small-cap assets, behave differently because relatively thin spot liquidity creates significantly higher price elasticity.

This is why KRW-denominated spot markets may become one of the most important indicators for the next altseason.

Kaiko data highlights Korea’s unique positioning.

During Q1 2024, KRW-denominated crypto trading volume across centralized exchanges reached approximately $456 billion, surpassing USD-denominated spot volume at roughly $445 billion.

KRW consistently ranked among the world’s top fiat currencies by crypto spot trading activity.

Kaiko also emphasized that Korean market liquidity remains heavily concentrated around Upbit and Bithumb, which together account for approximately 96% of domestic trading volume.

In other words, Korea is not a small regional market.

It is a highly concentrated source of KRW-denominated spot liquidity.

The composition of trading activity matters even more.

Kaiko’s analysis suggests that Korean trading activity remains overwhelmingly concentrated in altcoins rather than Bitcoin or Ethereum. According to recent estimates, KRW trading pairs account for nearly 30% of global spot crypto volume, while roughly 85% of Korean crypto trading activity focuses on altcoins.

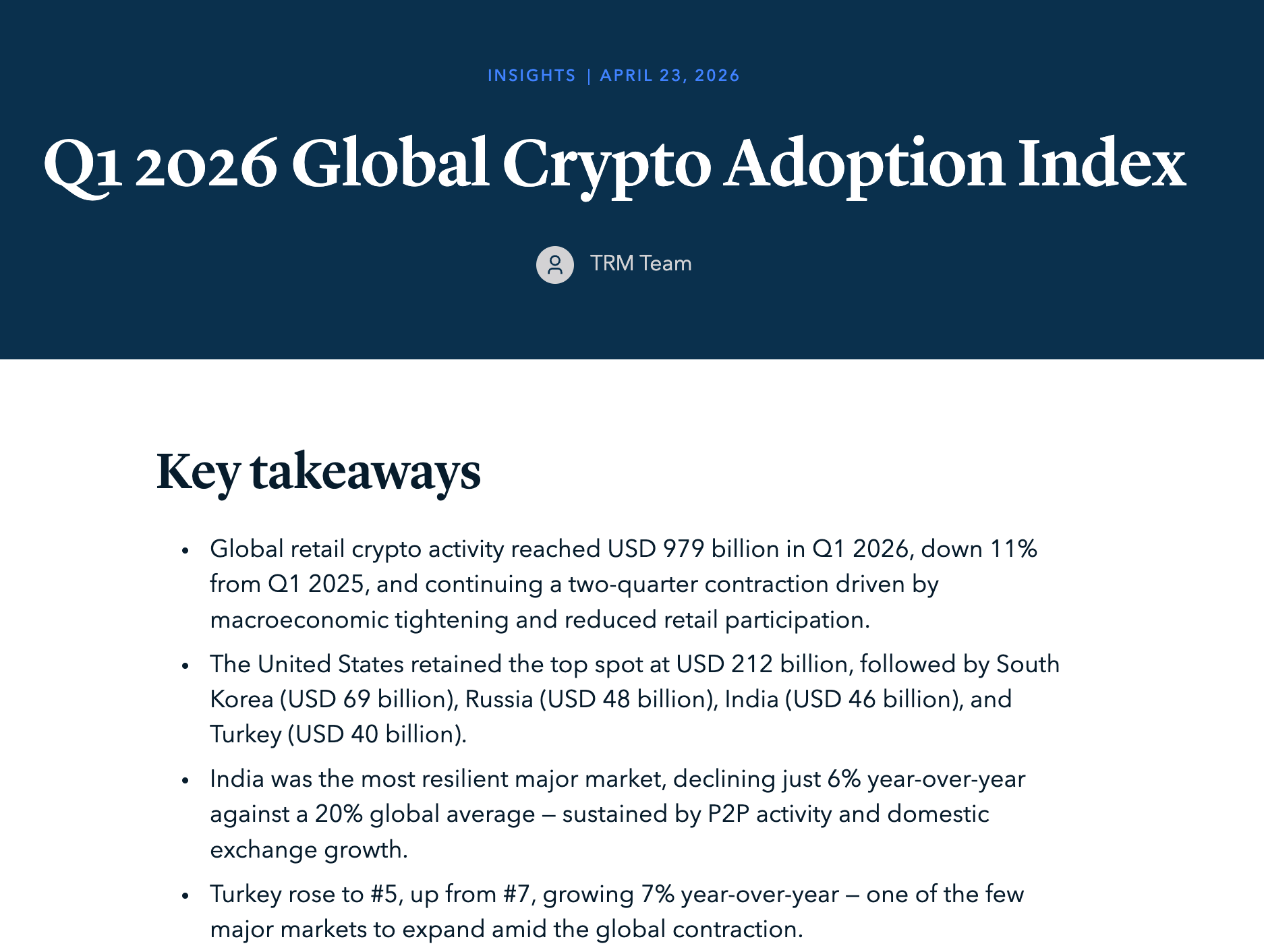

TRM Labs’ Q1 2026 global crypto adoption data reinforces this point.

Global retail crypto activity during Q1 2026 totaled approximately $979 billion, while Korean retail activity reached roughly $66.6 billion, ranking second globally behind only the United States.

Even amid declining global retail participation, Korea remains one of the world’s largest retail crypto markets.

Exchange-level data shows similar trends.

CoinMarketCap’s April 2026 exchange report estimated global spot trading volume at roughly $705.5 billion out of total crypto trading activity of $4.5 trillion.

Within spot-focused retail exchanges, Upbit continued maintaining meaningful global relevance.

Recent market concentration trends inside Korea are also notable.

While smaller exchanges lost significant liquidity during the KOSPI rally, remaining volume became even more concentrated inside major exchanges.

During May 2026, Coinone and Korbit saw trading volume decline roughly 78% and 92%, respectively.

Meanwhile, Upbit volume increased approximately 25%, while Bithumb volume fell only around 4%.

Combined market share between Upbit and Bithumb surpassed 97%.

This suggests that while total speculative heat weakened, the remaining KRW liquidity became even more concentrated within the largest trading venues.

Korean retail investors do not dominate global crypto markets overall.

But within altcoin spot trading, their influence is disproportionately large.

KRW markets maintain unusually high altcoin concentration, liquidity remains centralized within Upbit and Bithumb, and Korea continues to rank among the world’s largest retail spot trading markets.

As Bitcoin opens the upper range of the market and liquidity rotates toward large-cap altcoins, recovery in KRW altcoin trading volume across Upbit and Bithumb may become one of the clearest confirmation signals for the next altseason.

4. KOSPI 8,000 Is Not the Opposite of an Altseason

KOSPI 8,000 is the single most important variable in this report.

At first glance, it appears negative for crypto.

Part of the reason domestic crypto balances and trading activity declined is because Korean retail capital rotated into equities.

That much is true.

But interpreting KOSPI 8,000 purely as a competing asset class misses the possibility of delayed liquidity rotation.

The deeper meaning of the KOSPI rally is not simply equity strength.

It is the recovery of Korean retail risk appetite.

If investors were truly avoiding risk, it would be difficult for KOSPI trading volume and AI semiconductor equities to rally this aggressively.

Instead, capital has simply concentrated first in the most institutionally credible risk assets: AI semiconductor large caps.

On May 6, 2026, the KOSPI surpassed 7,000 for the first time in history before reaching 7,999.67 on May 12.

Samsung Electronics surged as much as 14.41% in a single day, while SK Hynix gained 10.64%.

This environment reflects Korean retail investors oscillating between FOMO and profit-taking pressure.

Of course, this rally cannot be explained by Korean retail investors alone.

Foreign capital and global hedge funds also played major roles.

As of May 7, hedge fund inflows into Korean, Japanese, and Taiwanese equities reportedly reached their highest levels in nearly a decade, with capital heavily concentrated around AI-related semiconductor and hardware companies.

Still, Korean retail participation remains important.

KOSPI 8,000 represents the convergence of global AI capital and domestic retail FOMO.

Even if institutions and foreign investors initiated the rally, late-cycle retail participants entering near local highs face a very different profit-and-loss structure.

If Samsung Electronics and SK Hynix eventually correct due to macro factors or institutional profit-taking, many late-entry retail investors may move into unrealized loss territory.

Behavioral finance becomes important here.

According to Kahneman and Tversky’s Prospect Theory, investors experiencing losses often become more willing to pursue higher-risk assets.

In other words, investors who suffer losses after chasing late-cycle momentum do not necessarily become defensive.

Some instead begin searching for higher-beta recovery trades.

In Korea, the capital rotation pathway is relatively predictable.

Liquidity initially concentrated in large-cap semiconductors can eventually rotate into KOSDAQ themes, AI, robotics, biotech, power equipment stocks, leveraged products, and ultimately KRW-denominated altcoins.

This path is particularly natural for investors who prioritize short-term momentum and turnover over long-term valuation investing.

For this reason, KOSPI 8,000 should not be viewed as evidence against an altseason.

In the short term, it absorbs crypto liquidity.

But in the medium term, it may function as one of the earliest leading indicators of renewed Korean retail risk appetite.

The key variable is not immediate substitution.

It is eventual high-beta rotation.

5. Which Altcoin Narratives Could Benefit Most?

1) The AI Semiconductor Narrative Can Expand Into Crypto

The rally in Samsung Electronics and SK Hynix is fundamentally driven by the AI growth narrative.

Importantly, this narrative is extremely intuitive for retail investors.

The improvement of generative AI is directly observable in daily life.

ChatGPT, Claude, Gemini, video-generation models, and workflow automation tools have transformed AI from an abstract theme into a visible consumer technology.

This naturally translated into semiconductor investment narratives.

Rising AI usage increases data center and GPU demand, which in turn drives HBM and high-performance memory demand.

As a result, Samsung Electronics and SK Hynix became viewed as direct beneficiaries of AI infrastructure expansion.

A similar narrative expansion can occur inside crypto.

Growth in the AI industry could increase demand for onchain data infrastructure, computation, verification, privacy, autonomous agents, and decentralized networks.

This does not mean every AI token possesses real utility.

Many projects remain heavily narrative-driven.

But during the early and middle stages of altseasons, easy-to-understand growth narratives often matter more than actual revenue generation.

Korean retail investors have already learned the framework:

AI growth → semiconductor beneficiaries

The next step could become:

AI growth → AI infrastructure, data, and agent-related crypto beneficiaries

If simplified investment narratives spread effectively through YouTube, Telegram, short-form content, and online communities, AI-related altcoins could generate disproportionately strong reactions inside KRW markets.

At this stage, narrative transmission matters more than technical superiority.

Korean retail investors embraced semiconductor momentum not because of detailed valuation modeling, but because the industrial growth story felt intuitive.

The same dynamic could emerge inside AI-related crypto sectors.

2) Tokenized Equities May Become the Most Intuitive Onchain Narrative for Korean Retail

Alongside AI, another major narrative likely to matter during this cycle is tokenized equities.

Korean retail investors already possess experience across Korean equities, U.S. equities, and 24/7 crypto markets.

Tokenized equities combine all three experiences into a single narrative.

The value proposition is relatively simple:

Global assets such as U.S. equities, ETFs, and commodities become tradable onchain, for longer hours, through stablecoin-based settlement.

Compared to complex DeFi structures or derivatives, this narrative is far easier for Korean retail investors to understand.

Investors already familiar with fractional U.S. stock trading, after-hours sessions, and overnight global equity access may naturally understand the appeal of 24/7 onchain equity markets.

Traditional finance is also increasingly moving in this direction.

ICE, the parent company of the NYSE, announced development of a tokenized securities platform capable of supporting 24/7 trading and onchain settlement.

The SEC has similarly emphasized that tokenized securities should not be treated as entirely separate from traditional securities markets.

In early 2026, the SEC stated that tokenized securities fundamentally represent existing securities in crypto-native form.

This matters because tokenized equities are not merely another crypto theme.

They increasingly represent the onchain extension of traditional financial infrastructure itself.

Ondo Finance represents one of the clearest examples.

Ondo Global Markets aims to bring traditional publicly traded securities onchain in tokenized formats usable within DeFi systems.

These products provide economic exposure linked to underlying public assets, including dividend-related returns.

Recently, Ondo GM surpassed $1 billion in TVL within tokenized equities.

This suggests that tokenized equities are evolving beyond pure experimentation into an asset category attracting meaningful capital.

xStocks represents another important example.

xStocks provides tokenized exposure to more than 100 U.S. equities and ETFs, including Apple, NVIDIA, and S&P 500-related products.

Since launch, xStocks reportedly surpassed $30 billion in cumulative volume and over 120,000 onchain holders.

These metrics suggest tokenized equities are generating real transactional and holding activity rather than existing purely as marketing narratives.

However, investors must still pay close attention to rights structures.

While tokenized equities may superficially resemble traditional stock trading, not all products provide equivalent ownership structures.

Some provide only synthetic economic exposure.

Others involve limitations around redemption rights, custody structures, voting rights, dividends, jurisdictional restrictions, or U.S. investor access.

Ignoring these distinctions could lead to severe misunderstandings around the tokenized equity narrative.

Nevertheless, from a narrative perspective, tokenized equities remain extremely powerful.

Korean retail investors are already familiar with both U.S. equities and 24/7 crypto trading.

Tokenized equities merge those two experiences.

If AI semiconductors represented “real-world beta for AI growth,” tokenized equities could increasingly become “onchain beta for global trading infrastructure.”

As a result, RWA, tokenized equity, and onchain securities infrastructure-related altcoins could occupy an important position within the upper narrative layer of the next altseason.

6. The CLARITY Act Could Compress Altcoin Discount Rates

One of the largest overhangs facing altcoins has historically been regulatory uncertainty.

Bitcoin secured institutional legitimacy through spot ETFs.

Altcoins, by contrast, remained burdened by uncertainty around securities classification, exchange listing risk, staking, airdrops, issuer liability, and protocol incentive structures.

That environment is gradually beginning to change.

On July 18, 2025, the United States formally enacted the GENIUS Act.

The White House described it as the first federal stablecoin regulatory framework in U.S. history, requiring full reserve backing and monthly reserve disclosures.

Meanwhile, the CLARITY Act has emerged as another critical variable.

White House digital asset advisers indicated that the administration is targeting roughly July 4, 2026 for progress on the bill.

This timeline should not be interpreted as guaranteed passage.

However, markets rarely wait for final legislation.

They begin pricing in expectations earlier through committee discussions, political signaling, compromise probability, and regulatory direction.

The evolving SEC and CFTC approach toward digital asset classification is also important.

Recent regulatory trends increasingly differentiate between categories such as digital commodities, stablecoins, collectibles, and tokenized securities rather than treating all tokens identically.

This effectively reduces the probability that every crypto asset will be treated as a security.

At the same time, tokenized equities and tokenized bonds remain more likely to be classified within traditional securities frameworks.

Importantly, regulatory clarity does not benefit all altcoins equally.

In fact, weaker tokens may face greater pressure.

Projects with opaque issuance structures or aggressive profit-sharing mechanics could encounter heightened regulatory risk.

However, large-cap infrastructure-focused altcoins may benefit from discount-rate compression.

If markets begin assigning lower probability to sudden regulatory classification risk, altcoins could experience greater beta expansion relative to Bitcoin.

This dynamic alone may not immediately trigger broad speculative rotation across smaller altcoins.

But it could function as a second-stage trigger following Bitcoin’s initial recovery, particularly benefiting large-cap infrastructure and institutionally explainable altcoins.

Over time, liquidity rotating into these assets could eventually spill further down into smaller KRW-denominated altcoins and low-liquidity speculative tokens.

7. 2026 Is the Final Full Pre-Tax Trading Year in Korea

Taxation is another uniquely important variable inside Korea.

Under revisions to Korea’s Income Tax Act, taxation on virtual asset income is currently scheduled to apply to transfers and lending activity beginning January 1, 2027.

This effectively makes 2026 the final full trading year before crypto taxation formally begins.

This is not simply a tax issue.

It is also a behavioral variable.

Korean investors have already experienced repeated debates around equity taxation, overseas stock taxation, and financial investment income taxes.

Crypto, by contrast, may increasingly be perceived as one of the final remaining high-beta asset classes operating under relatively favorable tax treatment.

If corrections emerge in large-cap KOSPI names and late-cycle retail investors begin searching for recovery trades, the psychological pressure associated with the “final pre-tax year” could further strengthen altcoin preference.

This matters not only for pre-tax returns, but also for expected after-tax asymmetry.

The possibility of an altseason in 2026 therefore extends beyond pure price momentum.

For Korean retail investors, crypto increasingly combines tax timing, 24/7 accessibility, volatility, and high-beta speculation into a single environment.

8. Venture Capital and Onchain Infrastructure Are Already Preparing for the Next Cycle

In May 2026, a16z crypto launched its new $2.2 billion Crypto Fund V.

This remains smaller than the $4.5 billion Crypto Fund IV raised in 2022.

But the significance is not the absolute size.

The significance is that large crypto-native venture funds are being raised again even while trading activity and altcoin sentiment remain depressed.

The 2022 cycle represented peak speculative overheating.

The 2026 environment increasingly focuses on infrastructure, productization, and long-term market architecture.

With Fund V included, a16z crypto’s cumulative capital commitments now approach roughly $9.8 billion.

Onchain infrastructure has also expanded significantly compared to prior cycles.

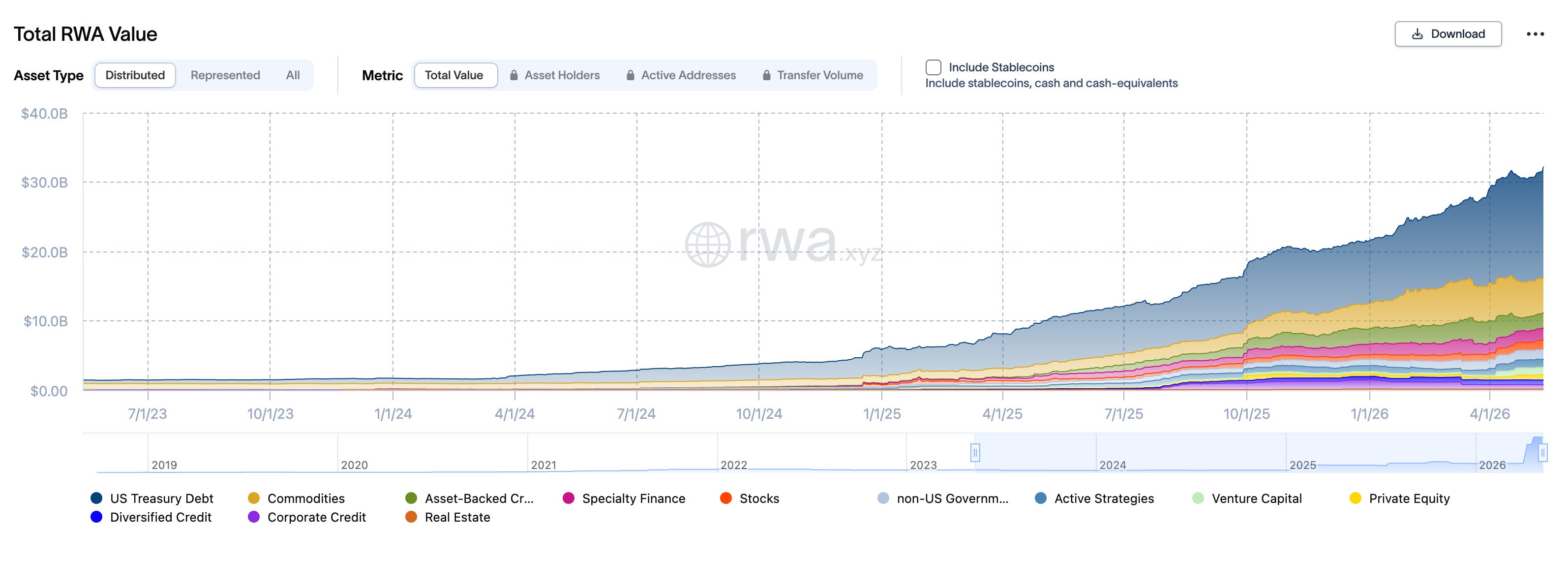

According to RWA.xyz, tokenized real-world asset markets across Ethereum, BNB Chain, Solana, Stellar, and other networks have already grown into multi-billion-dollar ecosystems.

CoinGecko’s RWA reports similarly noted that tokenized gold trading volume during Q1 2026 alone surpassed total volume recorded throughout all of 2025.

This cycle is no longer driven purely by exchange listings and speculative momentum.

CEXs, DEXs, perpetuals, stablecoins, RWAs, tokenized securities, and AI infrastructure are increasingly converging into a broader market structure.

More speculative behavior across smaller and lower-liquidity altcoins may still emerge in the later stages.

But the foundational infrastructure supporting this cycle is materially broader than before.

9. A Single Base Scenario

The altseason scenario outlined in this report is ultimately straightforward:

“Post-AI semiconductor rotation into KRW altcoin liquidity.”

This scenario unfolds across six stages.

Stage 1: Bitcoin Leads

ETF and institutional capital enters Bitcoin first.

BTC dominance remains elevated while altseason indicators remain low.

Markets interpret this as a Bitcoin-only cycle.

However, this stage does not contradict a future altseason.

Institutional capital naturally enters the deepest and most liquid asset first.

Stage 2: AI Semiconductor Rally and Korean Retail FOMO

KOSPI 8,000 emerges through the convergence of AI semiconductor momentum and Korean retail FOMO.

Samsung Electronics and SK Hynix become viewed as core beneficiaries of AI infrastructure expansion.

Korean retail investors directly participate in this rally, rebuilding overall risk appetite.

Stage 3: Large-Cap Corrections and Search for Higher Beta

If Samsung Electronics and SK Hynix eventually correct, many late-entry retail participants may move into unrealized losses.

Some capital rotates defensively.

But other investors begin searching for higher-beta recovery opportunities.

This rotation may flow into KOSDAQ themes, leveraged products, and KRW altcoin markets.

Stage 4: Recovery in Large-Cap Altcoins

As Bitcoin stabilizes and regulatory clarity improves, liquidity begins rotating into ETH, SOL, XRP, HYPE, and major AI/RWA-related infrastructure altcoins.

This stage is selective.

It is not yet indiscriminate altseason behavior.

Stage 5: Re-Ignition of KRW Altcoin Markets

As Korean retail risk appetite flows through KOSDAQ themes into KRW altcoin markets, trading volume across Upbit and Bithumb becomes the key confirmation signal.

KRW deposits and stablecoin balances remain inside the system.

The “final pre-tax year” dynamic also reinforces speculative participation.

At this stage, AI, RWA, tokenized equity, and stablecoin infrastructure narratives likely outperform first.

Stage 6: Smaller and Lower-Liquidity Altcoins

The final stage involves aggressive speculation in smaller and lower-liquidity altcoins.

Importantly, this is not the beginning of the altseason.

It is the confirmation stage.

Retail participants typically recognize the altseason only at this point.

From a research perspective, however, the true beginning occurs earlier, when KRW-denominated altcoin liquidity first starts recovering.

10. Risks and Key Variables

The largest risk remains a major Bitcoin drawdown.

Altseasons require Bitcoin stability.

If Bitcoin fails to maintain support near current levels and collapses sharply, liquidity rotation into altcoins would likely be delayed.

The second risk is prolonged KOSPI strength.

If Samsung Electronics and SK Hynix continue rallying without meaningful corrections, Korean liquidity may remain inside equities for longer.

In that case, the altseason timeline would shift later.

The third risk involves stablecoin interpretation.

Not all stablecoin supply represents speculative dry powder for altcoins.

Stablecoins also support payments, collateralization, settlement, and exchange operations.

Stablecoin market capitalization should therefore not be interpreted as entirely deployable speculative liquidity.

The fourth risk involves the selective nature of regulatory clarity.

Regulatory normalization does not benefit all tokens equally.

Some assets may actually face greater scrutiny.

Early beneficiaries are more likely to be large-cap infrastructure-oriented altcoins.

Conclusion: The Next Altseason Could Begin Inside Korean Retail P&L Psychology

The most important variable this cycle may not be Bitcoin itself.

Bitcoin has already opened the first door.

The more important question is what happens after Bitcoin.

Current data increasingly points in one direction.

Bitcoin has already absorbed ETF and institutional capital.

Altseason indicators remain low.

Global stablecoin supply exceeds $300 billion.

KRW exchange deposits and stablecoin balances remain inside Korea.

U.S. regulation is increasingly integrating stablecoins and digital asset market structure into traditional finance.

Korean crypto taxation is still scheduled for January 2027, making 2026 the final full pre-tax trading year.

And perhaps most importantly, KOSPI 8,000 confirms that Korean retail risk appetite has returned.

Previous altseason discussions focused primarily on Bitcoin dominance and global liquidity.

But this cycle increasingly requires analysis of Korean retail profit-and-loss psychology.

The AI semiconductor rally provided Korean investors with a directly understandable growth narrative.

Samsung Electronics and SK Hynix became “real-world AI beta.”

That same behavioral framework could increasingly transfer into crypto.

AI infrastructure, data, agents, privacy, and decentralized compute tokens may become positioned as “the next layer of AI beta.”

Tokenized equities matter for similar reasons.

Korean investors already understand Korean stocks, U.S. stocks, and 24/7 crypto trading.

Tokenized equities combine all three.

The familiarity of U.S. equities, combined with onchain accessibility and stablecoin settlement infrastructure, creates an unusually intuitive narrative.

Projects related to RWAs and tokenized equities, such as Ondo Finance, therefore deserve close observation.

However, investors must still carefully distinguish between rights structures, custody models, redemption mechanics, and economic exposure.

The next altseason will not arrive simply because Bitcoin rallied.

It may emerge because Korean retail investors are once again buying risk, and because that renewed risk appetite increasingly searches for higher volatility.

KOSPI 8,000 may represent the starting point.

Corrections in AI semiconductor large caps could place many late-entry retail investors into loss territory.

That loss-recovery demand may eventually rotate into KOSDAQ themes, leveraged products, and KRW altcoin markets.

As Prospect Theory suggests, investors experiencing losses sometimes become more willing to pursue higher-risk opportunities.

Korea’s unusually high retail turnover and strong altcoin preference could accelerate that process.

Therefore, the conclusion of this report remains straightforward:

The altseason is coming.

But its starting point will not be smaller speculative altcoins.

Bitcoin absorbs institutional capital first.

The AI semiconductor rally restores Korean retail risk appetite.

Large-cap altcoins and KRW markets respond next.

Smaller and lower-liquidity altcoins typically rally only after the broader altcoin cycle becomes obvious to the market.

The core battleground of the next altseason may not be global ETF markets alone.

It may increasingly become Korea’s KRW-denominated altcoin market itself.

Disclaimer

This material is provided for informational and research purposes only and does not constitute investment advice, nor is it intended to recommend the purchase, sale, or holding of any asset (including equities or tokens), or to replace independent investment judgment.

All views and analyses expressed herein are based on publicly available information and reasonable assumptions as of the time of writing, and are subject to change depending on market conditions, policy developments, or regulatory changes.

This research has been prepared independently and without any financial compensation, sponsorship, or incentives from any of the projects or their affiliated parties mentioned. However, the author or affiliated organization may have had prior commercial relationships with such projects, and potential conflicts of interest may exist. All opinions and interpretations presented in this material reflect the independent judgment of the author.

The final responsibility for any investment decisions rests solely with the reader. The author assumes no legal liability for any outcomes resulting from reliance on this content.

Terms of Use

Exilist permits the fair use of its research materials for non-commercial and informational purposes, provided that the original meaning and analytical context are preserved.

Proper attribution to Exilist is required when referencing or citing this publication.

Any form of republication, translation, modification, commercial distribution, or derivative use of this material, in whole or in part, requires prior written consent from Exilist.

Unauthorized commercial use, misrepresentation of analytical conclusions, or distribution without proper attribution may result in legal action.