Coinbase vs. Circle: Which Is the More Direct Beneficiary of U.S. Crypto Institutionalization?

How the GENIUS Act and the CLARITY Act create different premiums for stablecoin issuers and exchange platforms

This research compares the relative beneficiary structures of Coinbase (NASDAQ: COIN) and Circle (NYSE: CRCL) under two legislative developments: the GENIUS Act, enacted in July 2025, and the market structure bills in the CLARITY Act family, which had advanced to a meaningful stage of Senate discussion by 2026.

At the outset, one point should be made clearly. Greater regulatory clarity in the U.S. is structurally positive for both Coinbase and Circle, and the two companies have a complementary relationship within the stablecoin economy. This is not a comparison of pure competition.

What matters from an investor’s perspective, however, is not simply whether both benefit, but how directly that benefit translates into each company’s earnings and valuation. This piece is intended to compare exactly that: the relative directness and intensity of the benefit.

Executive Summary

Both the GENIUS Act and the CLARITY Act are legislative efforts pushing forward the institutionalization of the U.S. digital asset industry, and both Coinbase and Circle are beneficiaries of greater regulatory clarity. But these laws do not apply to them in the same way.

Coinbase (NASDAQ: COIN) is a comprehensive digital financial platform aiming toward the “Everything Exchange,” spanning exchange, brokerage, custody, onchain platform services, the Base network, and more.

Circle (NYSE: CRCL) is a company focused on stablecoin issuance, reserve asset management, and the expansion of payment and settlement networks.

What the GENIUS Act settled first was not the framework for exchanges or platform operators, but the framework for permissioned stablecoin issuers. In that respect, Circle is the company that entered the institutional framework first. Coinbase, by contrast, remains a company that must continue adjusting its trading, brokerage, custody, rewards, and tokenized asset strategy depending on the final language of the CLARITY Act.

The logic of stock price premium diverges here as well. Coinbase reported $6.883 billion in net revenue in 2025, of which $4.055 billion, or about 59%, came from transaction revenue. The company also discloses that its revenue remains significantly dependent on crypto asset prices and platform trading volumes. In other words, Coinbase is still a company whose performance is heavily influenced by market activity and the normalization of market structure. Of course, when the bull market returns and trading volume surges, its operating leverage can be extremely powerful.

Circle, by contrast, derived 96% of its $2.747 billion in 2025 total revenue from reserve income, and the company guided for 40% mid-to-long term growth in USDC circulation and an RLDC margin of 38% to 40%. In other words, Circle is a company whose upside is determined by stablecoin institutionalization and the resulting expansion in circulation.

Before comparing the value of the two businesses, one point must be emphasized. Coinbase and Circle are core partners in the USDC ecosystem. Circle is the issuer of USDC, but it does not monopolize the economics of the USDC economy. Through the Collaboration Agreement, Coinbase receives an economic share of Circle’s reserve income. In addition, Coinbase’s share of USDC platform holdings expanded from 5% in 2022 to 12% in 2023 and 20% in 2024. That means the current USDC economy is not a structure captured by Circle alone, but one built jointly by Circle and Coinbase.

If Circle grows, Coinbase grows with it. If Coinbase grows and expands USDC circulation and holdings on its platform, Circle’s reserve base and reserve income also grow. And when that income grows, Coinbase’s share under the Collaboration Agreement grows as well.

Even so, there is still a clear reason to assign a higher score to Circle in the current phase. It is more straightforward to identify which company connects policy benefit to earnings through the more intuitive path.

As stablecoin institutionalization deepens, the barriers to entry for issuers are likely to rise further. Permissioned issuer status, 1:1 reserves, disclosures and verification, and regulatory response capability are all required. In that structure, the issuer that enters the institutional framework first gains a first-mover premium. That is precisely where Circle’s strength lies.

At present, Circle is growing the USDC economy in a mutually beneficial relationship with Coinbase, and in the short term it still has a relatively high level of Coinbase dependence. Over the longer term, however, as more exchanges, fintech platforms, payment partners, and institutional settlement channels are onboarded, the reserve income generated by expanding stablecoin circulation connects more directly to Circle. In that process, dependence on any single partner can be relatively diluted. In addition, when issuer status is combined with seigniorage and economies of scale, Circle’s upside can extend well beyond circulation growth alone.

This is also visible in industry precedent. Tether, the issuer of USDT, is already a leading example of how profitable the stablecoin issuance business can be. Tether continues to generate overwhelming protocol revenue, while disclosing $13 billion in net income and $113 billion in U.S. Treasury exposure, demonstrating that reserve asset management is the core profit engine of a stablecoin issuer.

Circle is not merely an issuer that emphasizes profitability. It is an issuer that has also accumulated regulatory compliance and institutional suitability. As U.S. regulatory clarity and institutionalization advance in earnest, Circle is increasingly likely to secure a position not just as a stablecoin issuer, but as an unprecedentedly central issuer within institutional payment infrastructure.

1. Introduction

The U.S. digital asset industry has long grown under a structure in which legal definitions and supervisory frameworks lagged behind the pace of technological innovation. Exchanges, stablecoin issuers, custodians, and onchain infrastructure operators all faced a similar problem. It was often unclear which assets were securities, which were commodities, and which were payment instruments. As a result, companies operated under enforcement-based uncertainty, in other words, under a condition where regulators could later decide to challenge what they had already built. This was more than a legal problem. It translated directly into valuation discount.

But that structure began to change rapidly after 2025. First, the GENIUS Act was enacted, effectively defining stablecoins as a separate asset category under federal law. Then the CLARITY Act family of market structure bills advanced to the point where formal Senate review schedules were publicly announced. What matters here is not simply the general observation that regulation is arriving. The more important question is which regulation causes economic benefit to accrue where. Even the same regulatory clarity may not benefit a stablecoin issuer and an exchange in the same way.

Coinbase and Circle are the most appropriate comparison for this question. Both are frequently cited as major beneficiaries of U.S. digital asset institutionalization, but their business structures and earnings formulas are fundamentally different. Coinbase is a broad platform company spanning trading, brokerage, custody, institutional services, and onchain platform expansion. Circle, by contrast, is closer to stablecoin issuance, reserve asset management, and payment and settlement networks. As a result, even under the same legal environment, the form and intensity of benefit are bound to differ.

The key question is not which is the better company in the abstract, but which is more likely to receive the more direct institutionalization premium in a world where GENIUS is already in force and CLARITY is moving forward. To answer that question, this piece proceeds in the following order.

First, it reviews the U.S. regulatory landscape and the shift in investor perspective.

Second, it compares the business, financial, and asset structures of Coinbase and Circle.

Third, it examines the strategic significance of Base Network and Circle’s Arc.

Fourth, it reads Coinbase’s strategic horizon through the trajectory of Brian Armstrong, Coinbase’s CEO.

Fifth, it looks at the Korean case to assess the reproducibility of the power structure across stablecoin issuance, distribution, and usage, before summarizing scenario-based conclusions and the relative beneficiary structure.

2. Current Regulatory Landscape and Its Impact on These Companies

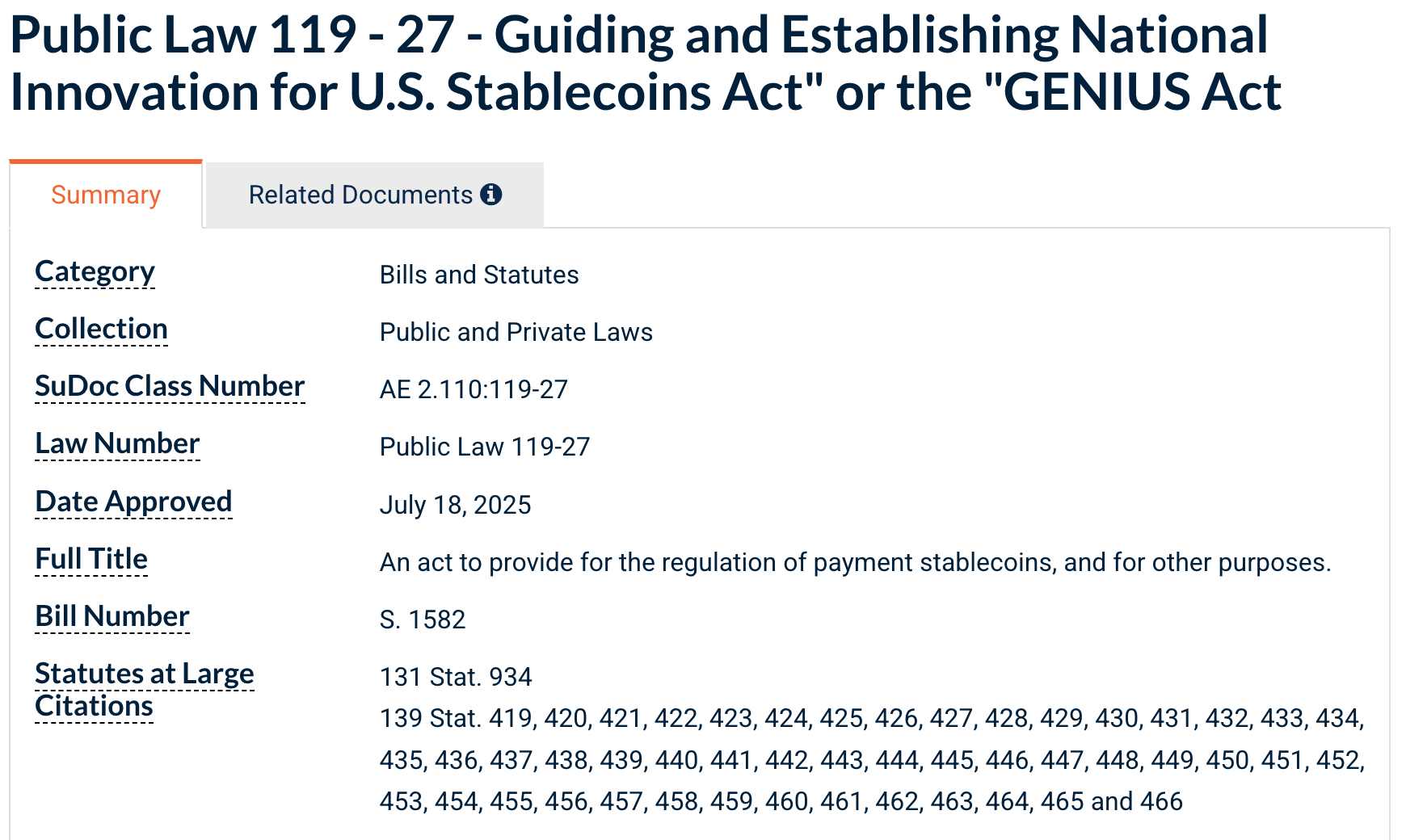

2.1 The GENIUS Act: Fixing Stablecoins as a “Rules-Based Payment Instrument”

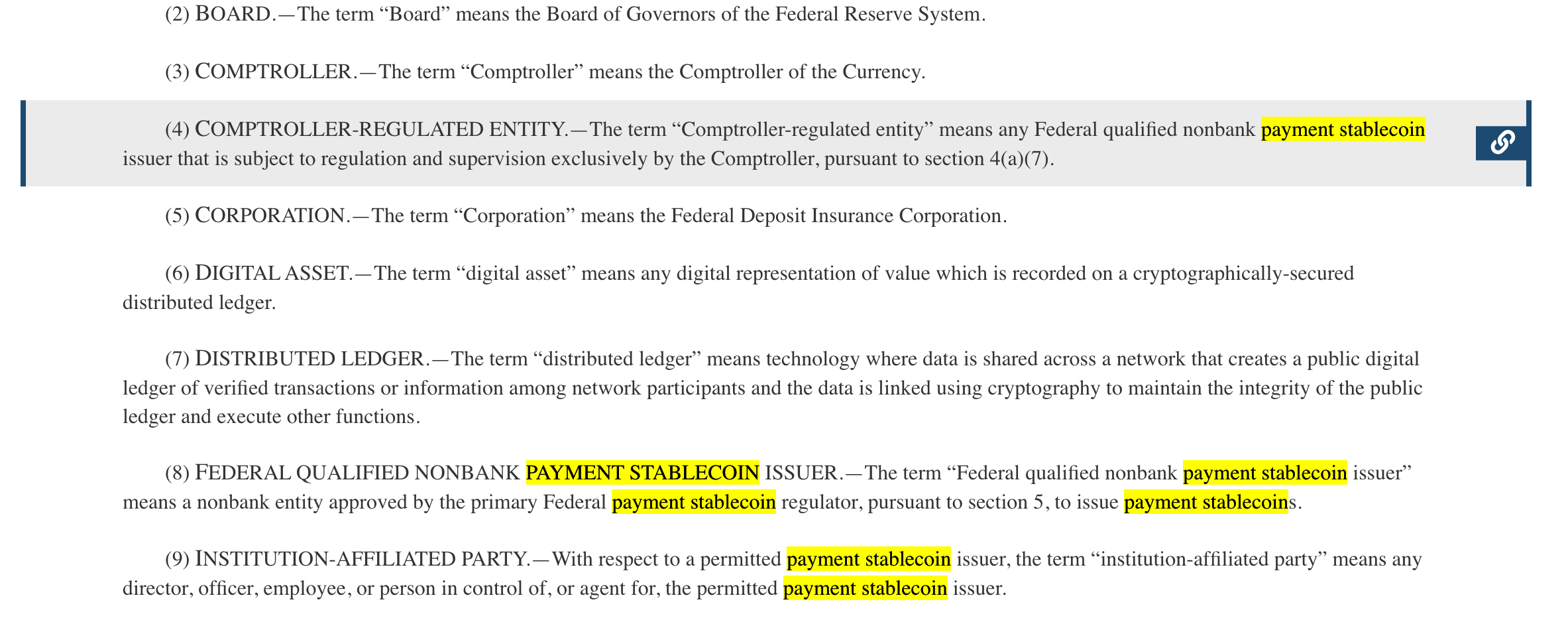

The core of the GENIUS Act is that it defines stablecoins not as mere private tokens, but as a separate federally recognized product category called payment stablecoins. The law brings together issuer qualifications, 1:1 reserves, permitted reserve asset scope, monthly disclosures, accounting verification, CEO/CFO certifications, and a prohibition on interest or yield merely for holding the asset into a single framework. This is a move that redefines the stablecoin industry not as a loose technological experiment, but as rules-based financial infrastructure.

The first effect of this law is the creation of an issuer bottleneck. Under the GENIUS Act, only qualified payment stablecoin issuers may issue payment stablecoins. In that structure, issuer status itself becomes an industry entry barrier. Issuance is no longer the private creation of a token that anyone can do, but a permissioned activity available only to firms that can support reserves and verification systems. This becomes a structural advantage for issuers like Circle, while strengthening issuer dependence for companies like Coinbase that are not issuers.

The second effect is the elevation of reserve asset management capability. The GENIUS Act limits reserve assets to cash, deposits, short-term Treasuries, RP/RRP, government money market funds, and similar instruments. This means reserve management is no longer simple safekeeping, but an activity that requires financial-infrastructure-level risk control and disclosure capability. The central competitive strength of the stablecoin business therefore shifts from “how fast can you attract users” to “how reliably can you manage reserves and prove that within a supervisory system.” This point connects directly to Circle’s business model, because Circle’s core earnings come precisely from reserve asset management.

The third effect lies in the direction created by the prohibition on interest and yield. The law bans interest or yield connected solely to holding, using, or maintaining the stablecoin. In practice, this means rewards received merely for holding the asset are to be blocked. This is a move to align stablecoins not as yield-bearing deposit substitutes, but as payment and settlement instruments. As a result, the basis of competition in the industry also changes. The key question becomes not who can offer higher holding rewards, but who can provide the more trusted payment instrument and distribution network.

The fourth effect is the restriction on DASPs, or digital asset service providers. The law establishes a structure under which, after three years, a DASP is generally prevented from offering or selling to U.S. customers any stablecoin not issued by a permitted payment stablecoin issuer. This increases the likelihood that stablecoin distribution in the U.S. becomes increasingly centered on permissioned assets over time. As a result, issuer premium rises, while distributors must redesign their strategies around permissioned assets. This structure has the force to reconfigure the market around issuers.

2.2 Latest Post-GENIUS Implementation: The Direction Is Already Set, and the Details Are Moving Into Rulemaking

As of March 2026, the GENIUS Act has moved beyond the legislative stage and into actual implementation. In September 2025, the U.S. Treasury issued an ANPRM asking for input on questions such as:

who should qualify as a “permitted stablecoin issuer,”

how far digital asset businesses such as exchanges and platforms should be included,

whether foreign-issued stablecoins should be recognized if they meet standards similar to those in the U.S.,

how strictly sanctions and AML rules should be applied,

and whether state-level regulations are sufficiently comparable to federal standards.

In plain terms, the broad direction has already been set by statute, and the process has now moved into determining how strict the detailed standards will be.

In March 2026, the OCC released a proposed rule for GENIUS implementation. The document further specified permitted activities, reserve and redemption standards, supervisory authority, and application procedures. The FDIC, after proposing section 5 application procedures in December 2025, also announced in February 2026 that it would extend the comment period and introduce additional prudential requirements. In other words, supervisory agencies have started designing the actual operating rules.

This is where the law begins to function as a system. The key question is who can turn this regulation from a cost into an entry barrier and competitive advantage. Circle may be relatively well positioned in this structure because it has long publicly emphasized a regulation-first posture. Coinbase, by contrast, is not an issuer, and therefore stands not as a direct operator of this law, but as a company that must redesign its distribution and service strategy on top of the framework it creates.

2.3 The CLARITY Act: A Law Intended to Create a Formal Route for Trading, Brokerage, and Custody

Unlike GENIUS, the CLARITY Act is intended to organize the broader framework for which assets fall under which regulators in the digital asset market, and how exchanges, brokers, and custodians can legally operate through formal procedures. Put differently, it is a law intended to define which assets can be handled under which licenses, and what structure trading and custody can take within the formal system. The key elements of the bill include the following:

the definition of digital commodities, or which coins can be viewed as having commodity characteristics,

joint rulemaking by the SEC and the CFTC,

permission for digital assets and permitted stablecoins to be traded not only on formal exchanges, but also on authorized alternative trading systems such as ATSs,

the creation of registration pathways for brokers, dealers, exchanges, and custodians to legally operate,

carve-outs for certain DeFi activities, meaning not all DeFi activity would necessarily be regulated,

and covered securities-related provisions, under which certain qualifying digital assets may no longer need separate registration in each individual state.

The significance of CLARITY is not simply that it is pro-crypto. More precisely, it is about moving uncertainty into the realm of predictability. A company like Coinbase has long been exposed to a structure where what is allowed and what is prohibited is contested after the fact. If CLARITY opens a clearer path, then it becomes easier to understand which products and services can be offered through which channels. That alone becomes a condition for a reevaluation of valuation multiples. If permissioned stablecoins and digital commodities can enter formal trading systems, then tokenized assets, hybrid trading, and institutional-grade digital markets can become real.

This connects directly to the realization of what Coinbase refers to as the Everything Exchange. In that sense, CLARITY could be a highly direct tailwind for Coinbase’s business expansion.

Even here, however, the benefit operates on the condition that trading infrastructure actually opens up. That is different in character from directly owning the key bottleneck of the stablecoin value chain. That leaves Coinbase exposed to procedural uncertainty, drafting volatility, passage risk, and amendment risk all at once.

On January 9, 2026, the Senate Banking Committee announced January 15 as the formal review date for digital asset market structure legislation. But on January 14, that date was postponed on the grounds that bipartisan negotiations were continuing. These two events reveal two things at once. First, the legislative discussion had risen to the level of an actual political timetable. Second, the final language remained unstable. In other words, the probability of passage increased, but amendment risk rose as well.

Reporting at the time identified tokenized equities, DeFi treatment, the CFTC’s role, and stablecoin rewards as major points of contention.

Brian Armstrong responded publicly by saying that Coinbase could not support the bill in its current form, adding, “We’d rather have no bill than a bad bill.” This signals that what matters more than regulatory clarity in the abstract is clarity that does not work against Coinbase’s earnings structure. Therefore, the most important issue in CLARITY negotiations is not the broad direction, but the allocation questions embedded in specific provisions such as rewards, tokenized assets, and state authority.

Opposition from state regulators is still ongoing. In January and February 2026, NASAA raised concerns in letters about the CLARITY and DCIA framework, specifically around covered securities, tokenized instruments, state antifraud enforcement, and the preservation of cooperative federalism.

State regulators are effectively arguing that while it is good for the federal government to organize digital asset rules, it should not go so far as to strip away too much state authority in the process. The stronger the push toward a single federal regime, the more favorable it becomes for large players. But in the Senate, concerns about the erosion of state authority can reappear in the form of demanded revisions. Coinbase is especially sensitive to these language changes because covered securities, ATS treatment, and broker-dealer-exchange registration routes matter directly to it. Circle may be somewhat less directly affected, but it is not immune, because the trading and distribution path of permissioned stablecoins is also connected to market structure. Therefore, the adjustment of state authority is not a side issue, but a key variable that could change the final shape of CLARITY.

3. The Business Positioning and Financial Performance of Coinbase and Circle

3.1 Not the Same Kind of Crypto Company, but Two Different Earnings Formulas

The difference between Coinbase and Circle begins with their earnings formulas.

Coinbase is a company that must be evaluated through trading volume, price volatility, product mix, user activity, regulatory pathways, and interest rates all at once. Circle is a company that must be evaluated through interest rates, USDC circulation, and distribution costs, meaning the partner allocation costs required to grow USDC. This is not a mere accounting distinction. It determines how regulatory benefit accrues.

CLARITY reduces Coinbase’s discount rate by organizing the trading market structure, while GENIUS creates an issuer bottleneck and raises Circle’s institutional standing. Coinbase is a company that can place more products and services on top of its platform when regulation opens up. Circle is a company whose core engine becomes stronger the more regulation defines stablecoins as permissioned payment instruments. From the perspective of how directly regulatory change connects to earnings, Circle has the shorter path.

3.2 Coinbase 2025 Results: Still a Transaction Revenue Company, but Now Deeply Linked to USDC Rates as Well

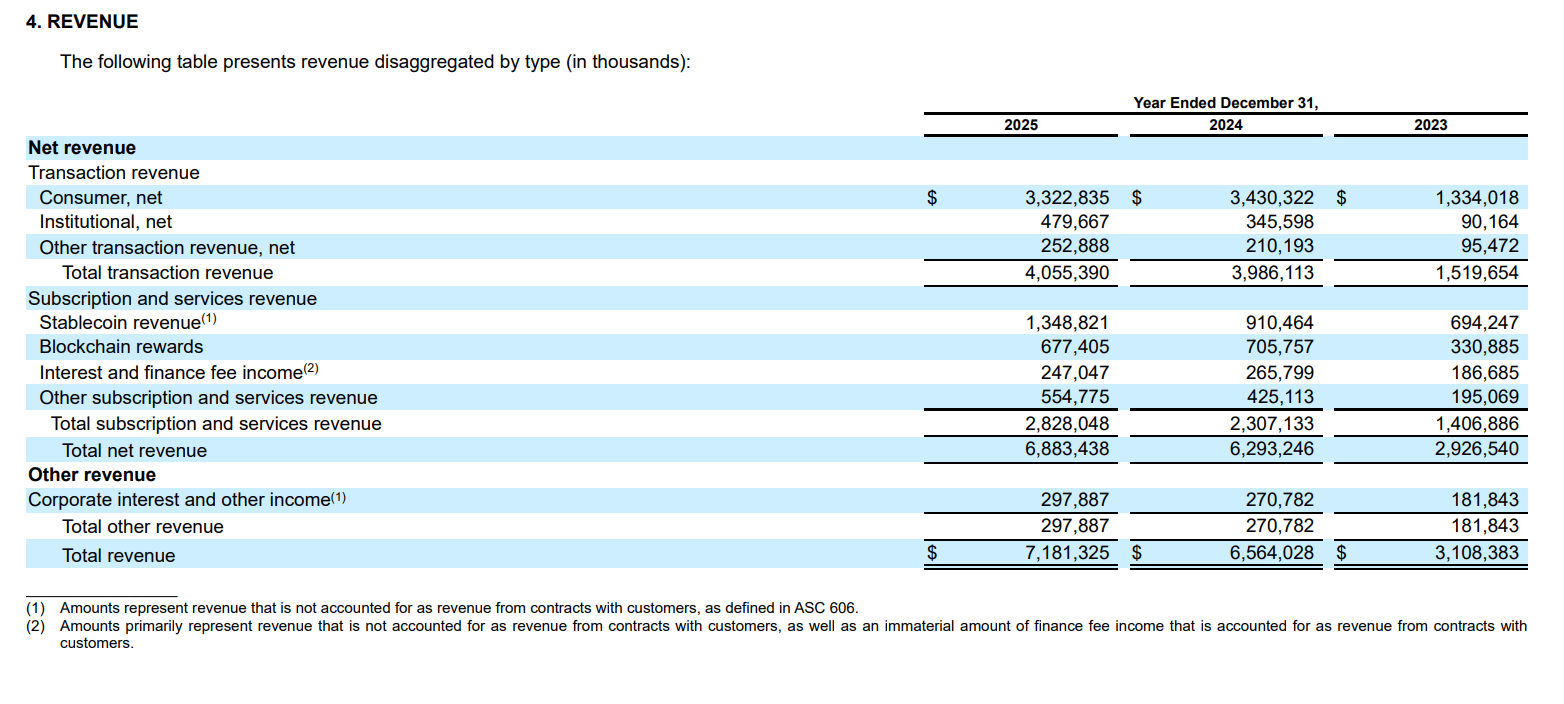

Coinbase’s 2025 10-K shows that the company is no longer limited to the exchange business.

annual trading volume: $1.221 trillion

assets on platform: $376 billion

monthly transacting users: 9.2 million

net revenue: $6.883 billion

transaction revenue: $4.055 billion

subscription and services revenue: $2.828 billion

Of Coinbase’s $6.883 billion in net revenue in 2025, transaction revenue accounted for $4.055 billion, or about 59%. Stablecoin revenue also grew to $1.349 billion, but the company discloses that its total revenue remains significantly dependent on crypto asset prices and platform trading volumes. It also disclosed that a 150 basis point move in interest rates could impact stablecoin revenue by as much as approximately $540.3 million.

This shows that while transaction revenue still exerts a high degree of influence, the notable point is that Coinbase is now deeply exposed not only to trading volume, but also to interest rates and stablecoin adoption. Coinbase is therefore both an exchange and a player in the USDC economy. That illustrates the company’s complexity. Its total assets were about $29.67 billion, with cash and cash equivalents, customer custodial funds, crypto investment assets, goodwill, and intangible assets all accounting for meaningful portions.

This is not a simple exchange. It is a structure that includes M&A, platform expansion, institutional services, and custody. For investors, that means both upside and burden. A broad business footprint means larger upside if the Everything Exchange becomes real, but it also means broader exposure to regulatory and macro variables.

3.3 Circle 2025 Results: Even More Clearly a Circulation × Rates Company

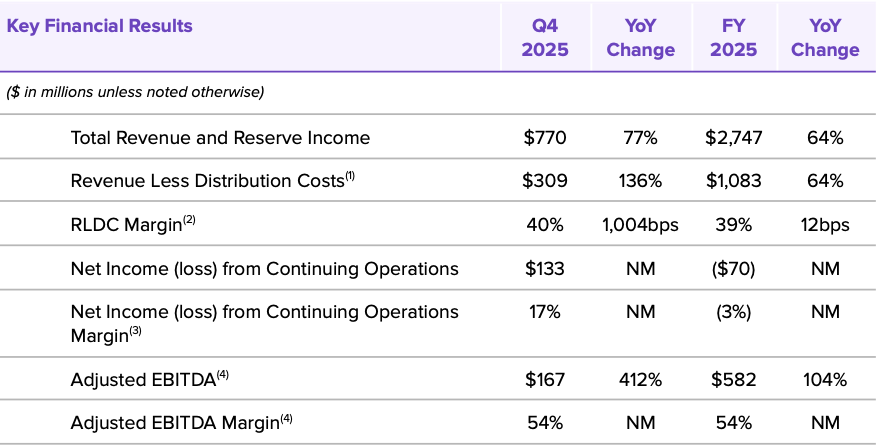

Circle’s full-year 2025 results more directly reveal the core of its business.

The company reported $2.747 billion in total revenue and reserve income in 2025, with reserve income accounting for 96% of the total.

USDC in circulation at year-end was $75.266 billion, and average circulation during the year was $64.870 billion. These figures make clear that Circle’s core formula is circulation × reserve yield.

There was a net loss, but the company explained the impact of IPO-related stock compensation, and adjusted EBITDA was $582 million.

What matters more to investors than a single line of net income is how clear the reserve-income-centered structure is. And the answer is clear. Circle’s earnings are much more directly connected to interest rates and stablecoin circulation than to broader market conditions.

Circle’s earnings formula moves simply as a function of circulation × interest rates. If CLARITY legalizes trading infrastructure and GENIUS elevates stablecoin credibility to an institutional level, the probability rises that stablecoins become the base unit of institutional payments and settlement. In that case, the most direct beneficiary is, of course, the issuer.

That said, falling interest rates are a direct hit to Circle. But Coinbase has also increased its stablecoin revenue mix and has disclosed interest rate sensitivity. Rate risk is now a shared variable for both companies. In that context, the company with more direct leverage to rising circulation is Circle.

In the balance sheet, segregated cash and cash equivalents held for the benefit of stablecoin holders make up most of the asset structure, which shows that reserve management itself is the core of the business model. This is structurally different from a typical platform business. Circle is more sensitive than a general platform company to declining interest rates, slowing circulation growth, sticky distribution costs, and the emergence of competing stablecoin issuers, rather than to user metrics.

3.4 USDC Economy Distribution: The Core Link Connecting the Two Companies

Coinbase and Circle are core partners that share the same USDC economy. Circle generates revenue through stablecoin issuance and reserve management, while Coinbase captures an economic share through USDC distribution, user touchpoints, and stablecoin revenue. The two companies therefore need to be analyzed separately, but the revenue distribution structure of the USDC economy must also be understood together.

The first thing that needs to be corrected is the oversimplified claim often repeated in the market that “Coinbase takes 50% of USDC-related profits.” According to Circle’s S-1, the Collaboration Agreement is not that simple.

First, a payment base is calculated after subtracting external management and custody fees and certain other deductions from reserve-generated income.

Then Circle takes an issuer retention amount first, reflecting the issuer role and related costs.

After that, Circle and Coinbase each receive a party product economics share based on the proportion of USDC holdings on their respective platforms.

And even after that, Coinbase receives 50% of certain remaining ecosystem economics from the payment base.

In other words, Coinbase’s economic share is not “50% of total USDC profits,” but a more complex structure calculated after multiple steps. Circle also recognizes the amount paid to Coinbase as distribution-related costs for accounting purposes.

This structure creates real synergy. If Circle grows and USDC issuance and circulation increase, the revenue Coinbase receives also rises. Conversely, if Coinbase grows and the amount of USDC held and circulated on its platform rises, Circle’s reserve base and reserve income also grow. And that increased reserve income is then shared with Coinbase again under the contract. In other words, the USDC economy itself is something the two companies are building together. In that sense, their relationship is closer to mutual amplification than pure competition.

The actual trend supports that interpretation. Circle’s S-1 states that on a 2024 daily weighted average basis, about 2% of USDC was held by Circle, about 18% by Coinbase, and about 80% by other third-party platforms. External analyses based on those disclosures also estimate Coinbase’s platform share of USDC holdings to have risen from around 5% in 2022 to 12% in 2023 and about 20% in 2024.

Looking only at the actual trend of the past few years, Coinbase’s influence within the USDC economy has been increasing. At the current stage, it cannot simply be assumed that as Circle grows, its Coinbase dependence automatically weakens. On the contrary, in the short term, Coinbase remains the strongest distribution and holding partner and occupies an even more important position.

That does not mean Circle’s upside is therefore more limited than Coinbase’s. The more important point is the directness of issuer premium after institutionalization. Today, the share of USDC held on Coinbase’s platform is a very important variable. But over the long term, Circle has the ability, based on its premium as a compliant issuer, to onboard more exchanges, fintechs, payment partners, institutional settlement channels, and FX networks. That means value can accumulate across a broader and more distributed set of channels. In other words, dependence on any one partner can be relatively diluted. Coinbase may be the largest USDC distribution partner today, but the current revenue-sharing structure may not be the final fixed end state in the long run.

3.5 Current Market Capitalization and Premium Relative to Financial Results

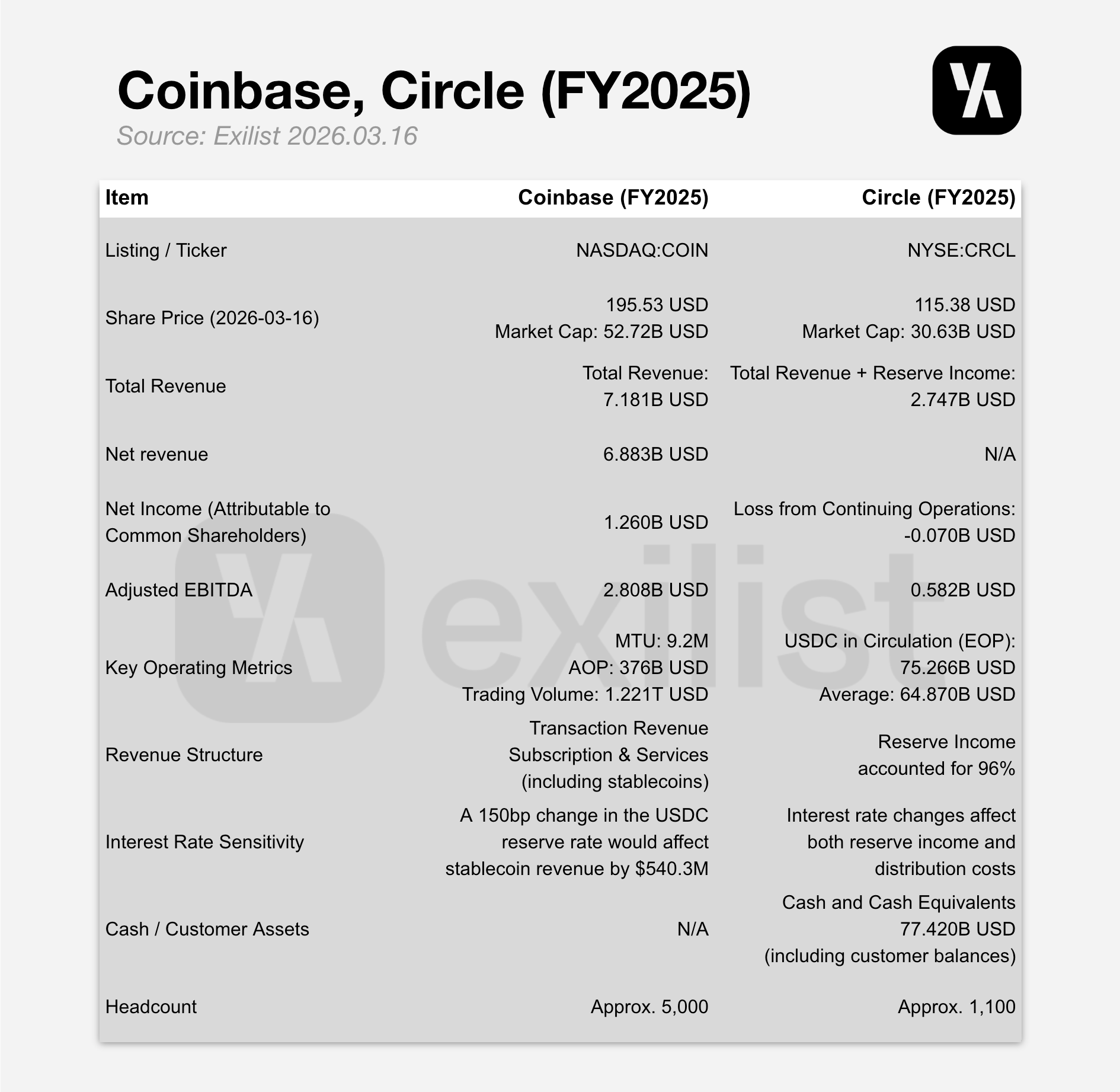

As of March 16, 2026, Coinbase (NASDAQ: COIN) had a market capitalization of $52.72 billion, while Circle (NYSE: CRCL) had a market capitalization of $30.63 billion. In absolute size, Coinbase is valued more highly. But rather than looking at the simple gap in market cap, it is more appropriate to compare how many multiples each company is trading at relative to its financial results.

Coinbase’s 2025 annual results were $6.883 billion in net revenue, $1.260 billion in net income, and $2.808 billion in adjusted EBITDA. On a simple basis, that implies Coinbase is trading at roughly:

7.7x revenue

41.8x net income

18.8x adjusted EBITDA

This suggests the market is valuing Coinbase not as a simple exchange, but as a platform company that includes trading, brokerage, custody, onchain infrastructure, and the Everything Exchange.

Circle’s 2025 annual results were $2.747 billion in total revenue and reserve income, a continuing operations net loss of $70 million, and adjusted EBITDA of $582 million. On that basis, Circle is trading at roughly:

11.1x revenue

52.6x adjusted EBITDA

Because Circle recorded a continuing operations loss in 2025 rather than positive net income, a P/E multiple is not meaningfully calculable. Accordingly, it makes more sense to evaluate Circle on reserve income structure and adjusted earnings, rather than on net income.

What this comparison shows is that in accounting-based valuation terms, Coinbase is indeed the stronger-quality company today. Coinbase trades at lower multiples relative to revenue and adjusted earnings and is valued as a platform company with clearly visible profitability. Circle, by contrast, is weaker on accounting profit but is being awarded higher expectations in terms of revenue and adjusted earnings multiples.

The market therefore appears to assign Coinbase a more stable platform premium, while assigning Circle a stronger expectation premium tied to stablecoin institutionalization. But from a business outlook perspective, Coinbase may already be a company whose platform profitability and diversification are largely visible, while Circle is still a company whose stronger earnings linkage to stablecoin institutionalization is being more heavily anticipated. That is precisely why the comparison remains worth making.

3.6 Scenario Comparison Based on Circle’s Guidance

Circle is a relatively narrow business, and its revenue structure is very clear. That can look like a weakness, but from an investor’s point of view it can actually be a strength. Unlike an exchange platform, where one must analyze trading volume, prices, user activity, product mix, and changes in legislative wording all at once, Circle’s core earnings formula is comparatively transparent. Interest rates remain hard to predict, but based on circulation, current margins, and cost structure, it is possible to estimate with some approximation how much earnings power the company could reach if its own guidance materializes. That is why Circle itself emphasizes RLDC, RLDC margin, and USDC circulation growth as key metrics.

Let us first look at the 2025 numbers.

Circle reported total revenue and reserve income of $2.747 billion in 2025.

Of that, reserve income accounted for 96%.

Total distribution, transaction, and other costs for the same year were $1.664 billion.

As a result, RLDC came to $1.083 billion, with an RLDC margin of about 39.4%.

RLDC is the amount left after subtracting distribution, transaction, and other costs from total revenue and reserve income. Put simply, it is close to the core earnings power remaining from the USDC economy after partner distribution costs are reflected. It is not the same as net income, but RLDC is arguably the clearest measure of how economically strong Circle’s core business really is.

These figures matter because Circle’s core operating strength has already reached substantial scale. Coinbase’s net income in 2025 was $1.260 billion. Of course, RLDC and net income are different concepts, so a direct comparison has limits. Coinbase’s net income reflects all operating costs, stock-based compensation, taxes, and non-operating items, whereas Circle’s RLDC is a pre-net-income measure of core profitability. Even so, the implication is clear. The core earnings power of Circle’s business is already approaching Coinbase’s annual net income in scale. In other words, the economics of stablecoin issuance and reserve management are operating at a far larger number than the market may fully appreciate.

From here, Circle’s own guidance can be expanded into scenarios.

The company has guided for approximately 40% annualized growth in USDC circulation over the mid-to-long term.

It has also guided for an RLDC margin target of 38% to 40%.

If this is applied simply to the 2025 average circulation of $64.87 billion, the next-stage average circulation would rise to roughly $90.86 billion.

If reserve yield does not collapse sharply, and if the cost structure, including distribution-related costs, remains broadly similar to that of 2025, then total revenue and reserve income could expand to about $3.85 billion, while RLDC could rise to around $1.5 billion.

That would imply core operating earnings power above Coinbase’s 2025 net income of $1.260 billion.

Circle’s strength, then, is not just the abstract idea that “it is attractive because it is the issuer,” but that once circulation passes a certain threshold, earnings power can accelerate sharply.

Even under a more conservative view, the implication does not really change. Circle’s core earnings formula is ultimately circulation × reserve yield × distribution structure. The hardest variable to forecast is interest rates. But even setting rates aside, when one considers the company’s guided USDC circulation growth alongside its current RLDC margin range, it is still relatively clear that the structure is one where core earnings power strengthens quickly as circulation increases. Compared with Coinbase, where one must simultaneously assess trading volume, prices, market sentiment, tokenized assets, and the final CLARITY language, Circle is far more legible through a simple numerical structure.

That does not mean Circle is always better than Coinbase. The counterarguments are also clear. First, Coinbase may have greater explosive upside in a strong bull market. If exchange activity, onchain fees, Base, tokenized assets, and the Everything Exchange are all re-rated together, Coinbase’s absolute upside may be larger.

Second, Circle shares the economics of the USDC ecosystem with Coinbase. An increase in circulation does not mean all of that incremental value remains with Circle shareholders.

Third, declining interest rates are a more direct burden for Circle. Coinbase is also exposed to rates through stablecoin revenue, but Circle’s core earnings formula is more directly tied to circulation and reserve yield.

Accordingly, in an environment defined by a strong bull market, a surge in trading volume, expansion in tokenized assets, and platform multiple rerating, Coinbase may be more favorable. But in an environment where issuer structure strengthens, USDC circulation expands, and payment and settlement infrastructure adoption becomes the center of gravity, Circle may be more favorable.

4. Base Network and Arc Network

4.1 Networks Targeting Different Markets

Both Base and Arc are open blockchain networks, but they differ in design purpose and in the markets they are targeting. That means it is more accurate to distinguish the growth criteria and actual competitors of each network than to compare them in a simple “which chain is stronger” framework.

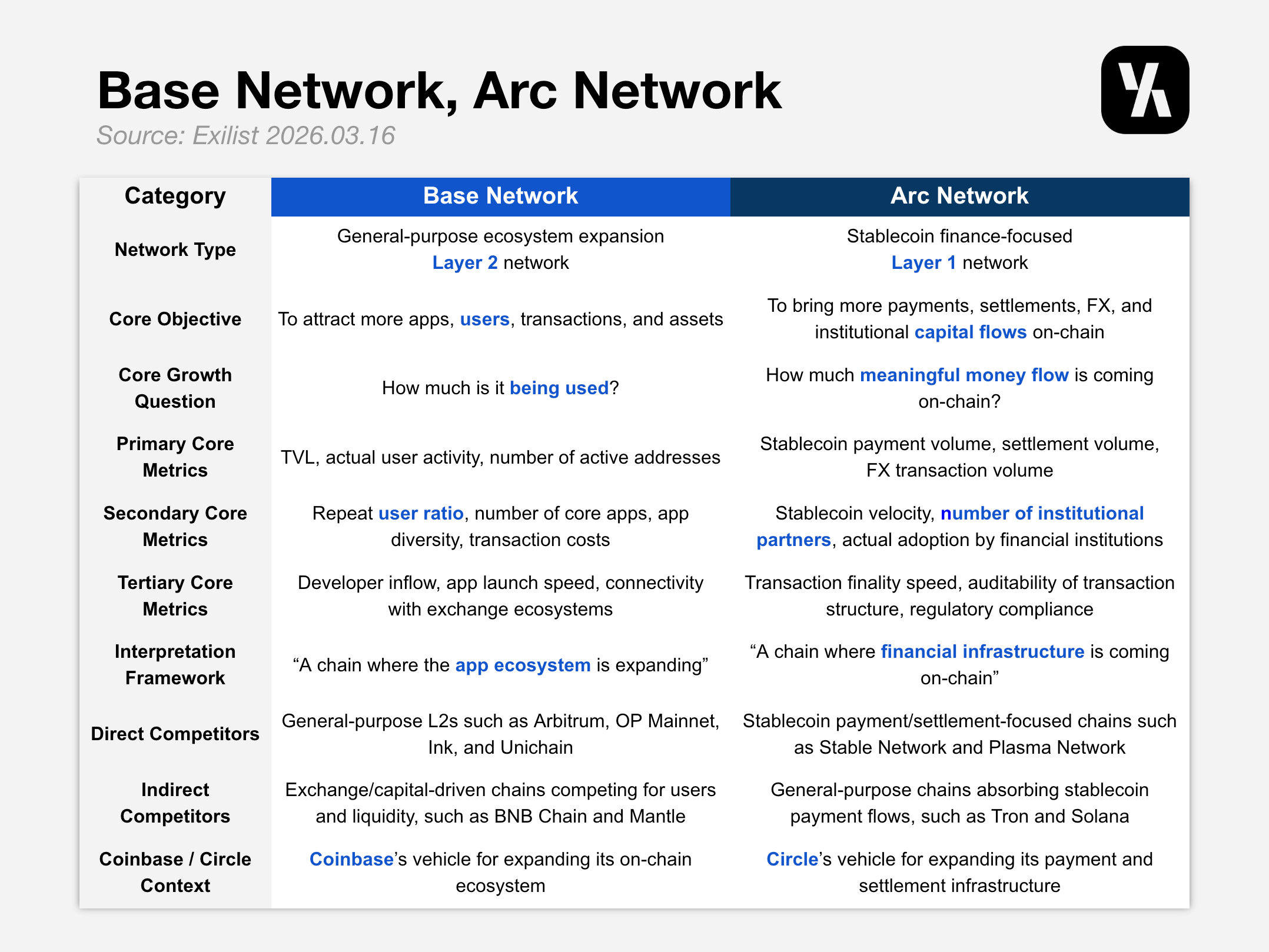

Introducing Base

Base is first and foremost a network for the onchain expansion of the Coinbase ecosystem. The Coinbase Sequencer receives, records, and reports transactions on Base, and in the early stage it operates as the sole sequencer. That is advantageous for fast operations and user experience optimization, but it also means trust in network operations remains more concentrated around Coinbase.

Base later announced the achievement of Stage 1 decentralization and the introduction of fault proofs in order to reduce this concentration risk. Taken together, it is more appropriate to understand Base not as a payments-specialized chain, but as a scalable Layer 2 network designed to grow a broader onchain ecosystem including apps, assets, and trading. Base’s current position supports that interpretation. As of March 2026, Base had approximately $11.46 billion in total value onchain and ranked among the leading chains in activity. In other words, Base is already establishing itself as a chain where people and applications are actually moving.

Arc | The Economic OS | Stablecoin-native L1 blockchain

Arc, by contrast, is a Layer 1 network for stablecoin finance. Circle presents Arc around several core elements: predictable dollar-denominated fees, sub-second transaction finality, optional privacy compatible with regulation, and direct connection to Circle’s broader financial infrastructure. Arc is a chain designed from the outset with payments, settlement, FX, and institutional financial applications in mind. It is less a general-purpose chain than a purpose-built financial infrastructure chain. That is the starting point for understanding the difference between Base and Arc. If Base is a chain designed to absorb more apps and user activity, Arc is a chain designed to move more important financial flows onchain.

4.2 Base’s Key Growth Metrics: User Activity, Capital Inflows, and the App Ecosystem

That difference leads directly to different views on which metrics matter most.

Because Base is an ecosystem-expansion network, its health and growth should be evaluated through metrics such as:

total value locked or total value onchain,

real user activity,

active addresses,

repeat user ratio,

number of core applications,

transaction fee levels,

and the pace of developer inflow.

The central question for Base is how many assets and how much activity are coming onto the network.

For a network like Base that is aiming for a broad application ecosystem, it is not enough to judge on TVL alone. Real transaction volume, app diversity, user retention, and fee competitiveness all matter together. Two chains can have the same TVL but very different quality if one has users returning frequently, balanced app growth, low fees, and active transaction flow.

4.3 Arc’s Key Growth Metrics: Payment Volume, Settlement Volume, Velocity, and Institutional Adoption

Arc is different. If Arc is viewed through the same lens as Base, centered on TVL or active wallets, the essence can be missed. Because Arc is a chain specialized for stablecoin finance, what matters far more than how much capital is sitting onchain is how often that capital is actually used in real payments and settlement.

The more important metrics for evaluating Arc are therefore:

stablecoin payment volume,

total settlement volume,

FX transaction volume,

stablecoin velocity onchain,

number of institutional partners,

actual case studies of financial institution adoption,

transaction finality speed,

and auditable transaction structure.

Base should be judged by how many people are using it, while Arc should be judged by how much important money flow is moving onto it. Velocity is especially important for Arc because it refers not to static balance size, but to how often stablecoins on the chain are actually circulating through payment, settlement, and FX flows. In that sense, Arc should be judged much more by payment network intensity than by TVL.

4.4 Base and Arc Are More Likely to Combine in a Synergistic Structure

Viewed this way, Base and Arc are more likely to combine as networks operating at different layers than to compete directly. Base is a network well suited for Coinbase to expand onchain user activity and the application ecosystem. Arc is a network well suited for Circle to connect stablecoins more deeply into institutional payment and settlement flows.

Base is stronger on the consumer, developer, DeFi, and application ecosystem side, while Arc is stronger on payment, settlement, and institutional financial infrastructure. Because the purposes of the two networks differ, they are more likely over the long term to become complementary within the broader USDC economy than to collide head-on for the same users. If Coinbase grows distribution, trading, and user touchpoints while Circle grows issuance, settlement, and financial infrastructure, then Base and Arc can also operate at different layers in a way that reflects those business structures. In that sense, it is more accurate to understand Base and Arc as networks serving different functions rather than placing them in a simple competitive frame.

4.5 Base’s Real Competitors: General-Purpose Ecosystem L2s and Exchange/Capital-Backed Chains

So who are Base’s real external competitors? Base should be separated from Arc at this point. Its most direct competitors are other ecosystem-expansion Layer 2 networks in the same category.

Specifically, Arbitrum, OP Mainnet, Ink, and Unichain are more appropriate direct comparisons. These networks all compete on application ecosystem, user activity, developer inflow, DeFi liquidity, and transaction cost competitiveness. Ink in particular, as Kraken’s OP Stack-based L2, is especially similar to Base as an exchange-built ecosystem-expansion chain. Base’s competition is ultimately about who can attract more users, more applications, and more onchain transaction activity.

Beyond that, BNB Chain and Mantle can also be viewed as practical competitors in a broader sense. Strictly speaking, they are not in the exact same Layer 2 category as Base, but they do compete for the same user capital and the same onchain activity, which makes them relevant comparison points.

BNB Chain has strong exchange-driven distribution power and a large retail user base that drive onchain trading and asset movement. Mantle’s strengths lie in its capital base, treasury size, DeFi asset attraction, and onchain financial narrative. In other words, even where the technical structures are not identical, BNB Chain and Mantle still compete for the same users, liquidity, and application ecosystems that Base is trying to attract. So Base’s external competitors are, narrowly, Arbitrum, OP Mainnet, Ink, and Unichain, and more broadly, exchange- and capital-backed chains such as BNB Chain and Mantle.

Even among those competitors, however, Kraken’s Ink is probably the most appropriate direct comparison.

4.6 Arc’s Real Competitors: Stablecoin Payment and Settlement-Specialized Networks

Arc’s real competitors are different. Arc should be compared not with general-purpose chains, but with networks whose core product is stablecoin payment and settlement.

On that basis, Stable Network and Plasma Network are more appropriate direct competitors for Arc. Stable describes itself as instant payment infrastructure based on USDT and emphasizes that it is a purpose-built network centered on fees and payment structure for stablecoins. Plasma likewise defines itself as stablecoin payment infrastructure, highlighting fast processing, low cost, institutional-grade security, and USDT-centric usability.

In other words, Stable and Plasma are not general-purpose chains built for broad user expansion. They are chains designed from the beginning for stablecoin payment and settlement, which makes them a much more accurate comparison axis for Arc.

One could also place general-purpose public chains like Tron in a broader competitive category given their large USDT usage, but fundamentally those remain general-purpose public chains. As such, they are less precise direct competitors for Arc.

4.7 Different Valuation Frameworks Must Ultimately Be Applied

From this perspective, the proper valuation metrics for Arc become clearer as well. If Arc is competing with networks such as Stable and Plasma, then it should not be evaluated based on TVL or simple active wallet count, but rather on stablecoin payment volume, settlement volume, velocity, FX processing scale, number of institutional adoptions, and the depth of integration with real financial infrastructure. Base, by contrast, should be judged through user activity, capital inflows, application ecosystem, transaction volume, and fee competitiveness.

Therefore, rather than grouping Base and Arc together as though they were the same kind of chain, it is much more accurate to analyze them separately according to the market each is targeting, the external competitors each faces, and the metrics appropriate to each. In summary, Base is an ecosystem-expansion chain that attracts applications, assets, and trading, while Arc is a financial infrastructure chain that connects stablecoin payment and settlement into institutional financial flows. The two are more likely to combine in a synergistic structure within the broader USDC economy over the long run. Their external competitors, however, are different. Base competes with general-purpose L2s and exchange- or capital-backed expansion chains, while Arc competes with stablecoin payment and settlement-specialized networks such as Stable Network and Plasma Network. This distinction is not just a matter of classification. It changes the core value metrics and the investment interpretation of each network.

5. Brian Armstrong’s Intent: How Far Does Coinbase Want to Go?

- Wikipedia")

Brian Armstrong’s messaging has followed a remarkably consistent pattern. He has continually called for regulatory clarity, indicated that Coinbase could invest more outside the U.S. if necessary, expanded political influence through efforts such as Stand With Crypto, and ultimately withdrew support publicly when the Senate market structure draft appeared unfavorable. This means Coinbase is not a company trying to avoid regulation, but one seeking regulatory clarity in a form favorable to its own strategy.

January 2023: internal messaging framed regulatory clarity as a long-term opportunity, maintaining long-term strategy even during the market downturn.

April 2023: comments suggested that if regulatory uncertainty persisted, Coinbase might invest more in overseas markets (“…we may have to consider investing more in other regions…”).

April 2023: during the SEC Wells Notice episode, he publicly argued that Wells Notices are not constructive when there is no clear rulebook (“…when there’s not a clear rulebook…”).

June 2024: Stand With Crypto, supported by Coinbase, grew rapidly, and Armstrong emphasized the expanding political influence of crypto users.

January 2026: when issues such as stablecoin interest and rewards restrictions emerged in the Senate draft market structure bill, Coinbase publicly declared that it could not support the current form, leading to the postponement of Senate Banking Committee discussion.

February 2026: Coinbase’s 10-K described its core 2026 vision as pursuing the Everything Exchange while simultaneously scaling USDC adoption (“…drive crypto’s role… through the Everything Exchange and by advancing stablecoin adoption…”).

As Coinbase’s 2025 10-K makes clear, the company’s central slogan is encapsulated in the phrases “Everything Exchange” and “advancing stablecoin adoption with USDC.” Coinbase has no intention of remaining merely a spot crypto exchange. It is trying to place trading, brokerage, custody, tokenized assets, onchain services, and USDC utility on top of a single platform. Base is the infrastructure pillar of that strategy, and CLARITY is the key law that could make it institutionally possible.

The public opposition in January 2026 is especially important. Armstrong said the bill in its current form was not supportable, adding, “We’d rather have no bill than a bad bill.” This means that what matters more than regulatory clarity in the abstract is clarity that does not damage Coinbase’s earnings structure. It also shows that specific provisions around stablecoin rewards, tokenized equities, and the role of the CFTC directly affect Coinbase’s interests. For investors, Armstrong’s statements become a kind of risk proxy. As CLARITY gets closer, Coinbase’s lobbying and political engagement may intensify, and with that the volatility of the bill’s final language may rise as well. But that is also one of Coinbase’s greatest strengths. The reason it reacts so sensitively is that if the bill is finalized in a way that favors Coinbase, the scope of expansion could be very large.

If everything unfolds according to the scenario Brian Armstrong is pursuing, spanning exchange, brokerage, custody, onchain services, USDC, Base, and the Everything Exchange, then the upside itself could ultimately be greater than Circle’s.

6. A Korean Coinbase-Circle Model? (Dunamu-Naver)

In Korea, won stablecoins are closely tied to monetary policy, financial stability, and payment infrastructure. As a result, key issues have emerged around the identity of the issuer, whether bank-centered or open to non-bank issuers, capital requirements, supervisory authority between the Bank of Korea and the Financial Services Commission, and whether interest should be permitted.

The U.S. Circle-Coinbase structure separates the issuer from the distributor or exchange. If won stablecoins become a reality in Korea, the central issue will likewise become who issues, who distributes, and who controls the places of use. This should not be read as a mere technical question, but as a restructuring of the power map.

At this stage of regulatory and legislative discussion, Dunamu (Upbit) appears to be moving beyond the exchange model and placing emphasis on infrastructure in the stablecoin era.

In this context, the recently announced GIWA is particularly interesting. The move to expand beyond the exchange into a chain and wallet suggests an attempt to capture distribution, settlement, and user touchpoints together. In U.S. terms, it is closer to a Coinbase + Base combination.

Naver affiliates, by contrast, are strong in payments and usage. Even if the issuer is ultimately determined to be a bank or consortium, the network of places where the stablecoin is actually distributed and spent becomes a separate source of power. In that case, the Circle-Coinbase-usage structure of the U.S. could be reproduced in Korea through a different combination.

Korea, however, differs from the U.S. in that policy risk is higher and the identity of the issuer has not yet been fully settled. But one thing is clear. If Korea also forms a structure in which the issuer is institutionally defined, then issuer premium will emerge, while distributors and usage networks will capture their own economic share on top of that. The Korean case should therefore also be read through the frame of an issuance-distribution-usage power structure. It should not be taken as a simple copy of the U.S. model, but as a clue for how that power map may reappear in Korea.

Conclusion

The core of this research is not to make a simple comparison of which company, Coinbase or Circle, is better. What matters more is identifying which company’s earnings structure is strengthened more directly as U.S. digital asset institutionalization advances, and which company is positioned closer to the center of that institutional change.

By that standard, both companies are clearly beneficiaries. Coinbase sits at the center of the order that the CLARITY Act is trying to define across trading, brokerage, custody, tokenized assets, and onchain platforms. Considering the structure that connects exchange, brokerage, custody, Base, and the Everything Exchange, the absolute size of the upside could be very large if market structure legislation is finalized in a way favorable to Coinbase. In particular, in an environment where a strong bull market, surging trading volume, expansion of tokenized assets, and platform multiple rerating all occur together, Coinbase is likely to show stronger elasticity.

But what the U.S. institutionalized first in this phase was not the expansion order of exchange platforms, but the order of permissioned stablecoin issuers. Through issuer qualifications, 1:1 reserves, disclosures and verification, interest prohibition, and distribution restrictions, the GENIUS Act first anchors the power structure of the stablecoin industry on issuers and reserve asset managers. And Circle is the company that entered that structure first. That is the single biggest divergence from Coinbase.

Coinbase is a company that can do more things once regulation is clarified. Circle is a company whose core business economics are directly strengthened as regulation is clarified. That difference is not small. Coinbase must simultaneously clear multiple variables such as trading volume, prices, rewards rules, the permitted scope of tokenized assets, and the final CLARITY language. Circle, by contrast, moves on a comparatively simple earnings formula built around circulation, reserve yield, and distribution costs. Coinbase is a company with more optionality, while Circle has a shorter path from policy change to earnings.

Of course, Circle does not monopolize the USDC economy. USDC is already an ecosystem strongly tied to Coinbase, and through the Collaboration Agreement Coinbase receives a large economic share of reserve income. Over the last several years, Coinbase’s influence within the USDC economy has not declined, but rather increased. So this research is not arguing for a simplistic issuer supremacy thesis that says Circle captures everything. Rather, the key question is who has the more direct institutional beta even within a structure where both grow together.

The answer to that question still leans toward Circle. As stablecoin institutionalization advances, barriers to entry for issuers are likely to rise further, and the premium for compliant issuers is likely to strengthen. Circle remains highly dependent on Coinbase today, but over the long term, as more exchanges, fintechs, payment partners, and institutional settlement channels are onboarded, dependence on any single partner can be relatively diluted. In that process, reserve income on growing circulation can accumulate more directly across a wider set of channels. In the end, Circle’s upside comes not simply from higher issuance volume, but from the combination of institutionalized issuer status and expanding reserve management scale.

For that reason, the final judgment of this piece is clear. Coinbase is one of the defining beneficiaries of the normalization of U.S. digital asset market structure. But Circle is the more direct and more pure beneficiary of stablecoin institutionalization. In periods defined by a strong bull market and explosive trading volume, Coinbase may be more favorable. But in the current phase, where GENIUS is already in force, CLARITY is still under negotiation, and issuer order is being defined first, it is more reasonable to view Circle rather than Coinbase as the company to which the core economic pool of policy change is more directly connected.

Legal & Disclosures

Disclaimer

This publication is for informational and research purposes only and does not constitute investment, financial, or legal advice, nor a recommendation to buy, sell, or hold any asset.

All analysis reflects publicly available information and reasonable assumptions at the time of writing and may change as market or regulatory conditions evolve.

This research was prepared independently and without compensation from any issuer or affiliated party. Readers are solely responsible for their own investment decisions. Exilist assumes no liability for any losses resulting from reliance on this publication.

Terms of Use

Exilist permits the fair use of its research materials for non-commercial and informational purposes, provided that the original meaning and analytical context are not altered.

When referencing or citing this publication, clear attribution to Exilist is required.

Any republication, translation, restructuring, commercial distribution, or derivative use of this material, in whole or in part, requires prior written consent from Exilist.

Unauthorized commercial use, misrepresentation of analytical conclusions, or redistribution without proper attribution may result in legal action.